All the way from America: What’s the best withdrawal strategy in retirement?

by Doug Brodie

/1. S&P500 – like Tiffany it’s expensive though is it value for money?

I spoke with a client a couple of months back as he was heading off on holiday: “I’m taking all three Rolexes with me”. The cost of those will not surprisingly be equal to someone’s mortgage. Now the owner, a successful business man who has recently sold his lifetime company, loves the value it brings to him and his new, retired lifestyle. The point is that there are many ways to value something and only one cash cost.

The S&P500 has been driven skyward over the past recent years by the Mag 7 – it’s p/e ratio is one measure equity value, in summary it tells you how many years’ profit makes up the share price. If a company has a p/e of 8 and the profit is £1m then the company is valued at £8m. If its main competitor has a p/e of 12, then that same £1m profit values that company at £12m making more expensive than its chum. The S&P collates the p/e ratios of its constituents, and today it’s p/e is 28, and that’s higher than the long term average in the chart, but not hugely so.

You can see the spikes at 2000, 2008 and 2020 when the p/e ratios went skywards – that is because the share prices fell through the floor, yet the profits were still measured as the same. At 28, we see a similarity to the 2-3 years lead up to 2000, so we think there’s still some time before the correction. However we also know that it is geopolitical shocks that crash markets and blimey, there’s a lot of potential for that just now.

Ultimately we think there’s a big correction coming for the US, when the valuations will revert to mean – they will fall back to average long term values. The trading trick is knowing when.

/2. It’s not about the money: a grown up in America.

You’re not ‘old’ you’re ‘older’.

A slightly awkward truth is that as you read this you are as young as you’ll ever be. You don’t need to be as un-thin or un-fit as you’ll ever be - a spot of exercise and calorie control will deal with those. However as Cher reminded us, we can’t turn back time.

I was shooting a video this morning with a chap from Vanguard in the US who has a PhD in Behavioural economics. Most of the reality that our clients see in our process, he has a label for – think of the black & white pictures, the annual cashflow projections, the slide rule etc. One of the items he and his team identified is the issue created by spending a working lifetime watching our values creep up and taking pleasure every time values grow: then at retirement we/you have to switch off that part of your mindset, and recognise a different aspect, and that’s successful decumulation.

Charlie Munger, 2019

The grown up in the room

“Well, I have an attitude that’s entirely different from our president’s. I am glad that we ran a big trade deficit with China, that enabled them to rapidly get out of poverty and obscurity. I welcome the Chinese to the group of advanced nations, which I think we enabled considerably by our willingness to trade with them as they moved ever upward in terms of complexity of enterprise. So I like what’s happened. I don’t regard it as unfair and bad.

I’m not saying that it would be unthinkable to have some tariffs somewhere, but basically I’m a free trader. And I’m particularly a free trader in dealing with China. I like the fact that free trade with China has enabled China to expand so much. They got out of poverty. They had hundreds of millions of people in rural poverty. In the whole history of the world, no big nation has ever advanced faster than China - and this free trade helped them do it. I like it.”

/3. The Pension Revolution: Doug Brodie & George Aliferis live on YouTube.

George Aliferis is a blogger, YouTube and content creator working in the financial space. George’s background was doing it the long way round and actually working for investment banks so he is pretty insightful in this area.

My interview by him covered the present pension revolution, the kicking in of the mass decumulation era, the pension time of the boomer generation.

Ok boomer.

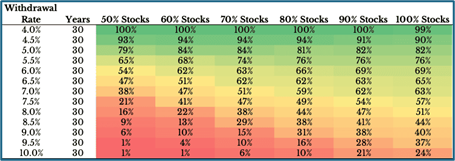

/4. All the way from America: What’s the best withdrawal strategy in retirement?

It’s all in the data; the markets are the same for you, me, the big guys, the hedge funds, the Rolls Royce pension fund. My £1 is the same as your £1 and her £1 – it’s we who make the differences to our own pounds, and in retirement there are right ways to draw down money and not-so-right ways.

A simpler way to look at the problem

Think of your retirement pot like an orchard:

· Fruit = dividend income: Every month the orchard naturally produces £1,600 of fruit for you to eat (spend).

· Trees = fund units: To cover the extra £400 you need (so you still have £2,000 to live on), you occasionally chop down and sell a few trees.

Now imagine a violent storm that instantly knocks 25% off the value of every tree.

Before the storm each tree fetched £4. You only had to chop 100 trees to raise £400. After the storm each tree is worth just £3. You must now chop 133 trees (one-third more) for the very same £400.

Because you have fewer trees left, next year’s fruit harvest will also be smaller, forcing you to fell even more trees. If bad weather lasts, this can turn into a vicious circle: selling ever more trees to pay the bills until the orchard can’t recover.

That danger is called sequence-of-returns risk (often shortened to sequence risk).

Key takeaway

It’s not just how much your investments earn that matters in retirement, but when they earn it. Large losses (or even modest losses combined with regular withdrawals) early on can snowball into long-term damage. Techniques such as keeping a cash buffer, lowering withdrawals in bad years, or using investments that pay steadier income can help keep the orchard healthy for longer.