Blood on the tracks

by Doug Brodie

[1] Owning a business, not trading a screen

There is a quiet but important difference between investing and trading, and it is one I find myself explaining at kitchen tables up and down the country. A trader buys a share hoping to sell it to someone else for a little more next week. An investor buys a small piece of a real business, its factories, its brands, its customers and its profits, and then settles in to share in the rewards of ownership.

Warren Buffett put it plainly in his 1996 letter to shareholders:

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”

Years earlier he had written that his favourite holding period was forever. He was not being lazy. He was reminding us that the value of a good company is built slowly, through years of selling more, earning more, and paying more out to its owners.

When you think like an owner, the daily wobble of the share price matters far less. You stop asking what the market will pay you tomorrow and start asking whether the business is still sound. That shift in mindset is, in my experience, the single most settling thing a retired investor can do. You are not a punter watching a screen. You are a part-owner, drawing your income, and letting the years do the heavy lifting.

[2] The cost of living, and the price of a ski pass

We hear a great deal about the cost of living in Britain, and it is real enough. But it is worth remembering that the squeeze is felt right across the wealthy West, and sometimes in places that might surprise you.

Take skiing, a holiday close to many retired hearts. A single day’s lift pass at a big all-in Colorado resort now sits at around $250, and at the very top end the peak-season window price at Vail has reached $356 for just one day on the mountain, the highest ever charged at an American resort. Add American food, drink and accommodation on top, and a week soon becomes distinctly distracting.

Set against that, flying into Switzerland or France can genuinely work out cheaper for a week’s skiing, even after the airfare. A European pass for a full week often costs less than two or three days in Colorado, and lunch on the terrace will not need a second mortgage.

I mention this not to plan your holidays, but to make a wider point about retirement spending. Prices are not fixed, and they are not the same everywhere. A little flexibility about where and when you spend can stretch your money a long way. The cost of living is high, yes, but it is also surprisingly negotiable if you are willing to look further afield.

[3] “You don’t make that kind of money selling bibles.”

“You don’t make that kind of money selling bibles” is a flippant line, but it captures a serious and increasingly tangled question: what counts as a harmful investment, and what counts as a social good?

For years the answer felt simple: tobacco, gambling and weapons went in the avoid pile, and the rest was fair game. That neat division has frayed. Since Russia’s invasion of Ukraine, a number of fund managers have quietly decided that defence belongs to the S for social in responsible investing, on the grounds that a nation unable to defend itself protects no one. In March 2025 Allianz Global Investors began allowing defence companies into funds with binding sustainability criteria, and the European Commission confirmed that investing in defence is compatible with its sustainable finance rules.

Then there is the awkward middle ground. Is a jet engine maker such as Rolls-Royce good or bad when the very same engines power both the airliner taking your grandchildren on holiday and a military aircraft? I do not think there is a clean answer.

My point is not to tell you what to think, but to warn gently against easy labels. Ethical and sustainable are not the same thing, and a fund’s badge tells you less than its actual holdings. If these things matter to you, and for many they do, look under the bonnet rather than trusting the sticker on the windscreen.

[4] You are not the average

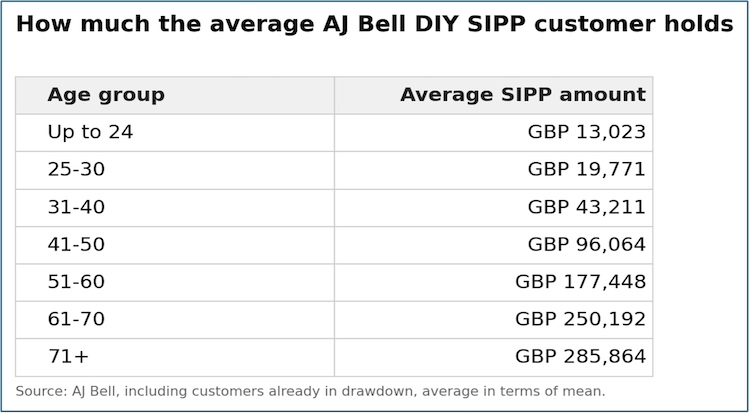

AJ Bell has published the average self-invested personal pension held by its do-it-yourself customers, broken down by age, and it makes for interesting reading. The averages climb steadily with age, from around £96,000 for those in their forties to about £286,000 for those aged 71 and over.

Average DIY SIPP held on the AJ Bell platform, by age band (mean, including customers in drawdown).

Look at the last step in the table. The over-70s hold on average around £285,864, against £250,192 for the 61 to 70s, a difference of £35,672. These are different people rather than the same savers followed through time, so we should not read too much into it, but the pattern hints at something cheering: many in their seventies still see their pots grow faster than they draw on them.

Now the gentle caution: an average is a single number doing an enormous amount of work, and it hides huge variation. Half of these savers hold less, some a great deal less. If your own pot looks nothing like £286,000, please do not despair. You are not the average, and you were never meant to be.

The useful lesson is the direction of travel, not the headline number. A well-invested pension can keep growing well into later life, quietly outpacing the income you take from it. That, in the end, is exactly how a retirement ought to feel.

[5] Remember Sid, and remember mean reversion

Remember Sid? In December 1986 the government floated British Gas with the cheerful “If you see Sid, tell him” campaign. Around four million people applied for shares, many buying stock for the very first time, and Britain gained one of the largest share registers in the world.

The noise around the SpaceX flotation, reportedly the largest stock market listing in history, brought Sid back to mind. The early money in such deals comes from those who can write a one billion dollar cheque without blinking, Middle Eastern sovereign funds among them, because for them it is a multi-generational bet whose rewards may only be seen long after our graves have turned to dust. It is not designed for Jane Mainstreet with £10,000 in her ISA, or Harry Highroad with £20,000 in his SIPP. (These flotation details are very recent and still moving, so do please check the latest before acting.)

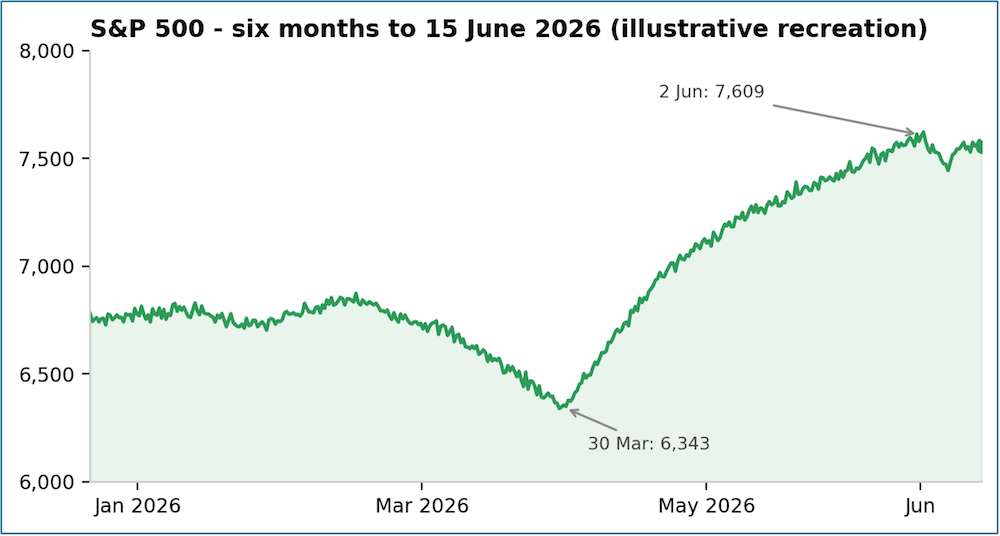

Now the part nobody enjoys. Markets revert to the mean. Look at the chart below. The S&P 500 climbed from 6,343 on 30 March to a peak of 7,609 on 2 June. Here is the working:

7,609 minus 6,343 is 1,266 points.

1,266 divided by 6,343 is 0.1996, just under 20%.

That gain came in about nine weeks, which is 9 divided by 52 weeks of a year, or 0.173.

20 percent divided by 0.173 is roughly 115% a year.

S&P 500, six months to 15 June 2026. A recreation of the supplied chart, with the 30 March low and 2 June peak marked.

A return of 115 percent a year cannot last, and it will not. After the dot-com mania, the NASDAQ peaked in March 2000 and then fell about 78 percent over the following two and a half years. I cannot tell you when the tide turns, because I do not know, but mean reversion is not a theory, it is gravity, and it collects in the end. The only sensible question is whether you are ready for it.

Been here, seen this before; trust derived income is insulated from market falls – you do not receive dividend income from the capital assets of an investment trust, you receive it from the revenue reserves.

About the author

Doug Brodie is Founder and CEO of Chancery Lane Income Planners. He has specialised in retirement income for over thirty years and is Chartered with both the CISI and CII. This article is general information and not personal advice. Tax rules can change, and the impact of any planning depends on your specific circumstances. Capital is at risk and past performance is not a guide to future returns.