Don’t go chasing short cuts

by Doug Brodie

/1. Avoid the errors others make.

Regulate your financial emotions

The picture above: Ravi Saini was a 10-year-old lad when he went to Scarborough beach with his family in 2020; he got out of his depth and was pushed from shore by the current. From something he'd watched on TV, he simply rolled onto his back and let the tide take him where it would, and an hour later he was scooped up by an inshore lifeboat.

As an adult experienced open water swimmer and diver, I know how unbelievably quickly a strong current dissolves every last ounce of energy in your body, swimming against tides being the only time I have known complete and total exhaustion.

“When the market turns against you, do not try and swim against the tide, float on top.”

Invest in removing pension anxiety: do not be afraid of taking advice

The 30-year-old version of you had very different priorities and a completely different financial life. At 40 (or 50), life often looks like a juggling act - mortgages, car loans, credit cards, family responsibilities - all accompanied by that constant whisper: “I should really be saving more.”

Back then, the goal was simple: build capital. Make regular monthly investments. Add the occasional lump sum when you could. Keep things moving forward.

Now, the focus shifts. It’s no longer just about building - it’s about protecting what you’ve built and turning it into an income that keeps pace with inflation and lasts well beyond your lifetime. The capital is what it is. And when people are disappointed with where they’ve ended up, we often see two reactions:

They avoid speaking to a professional planner because they worry they’ll be judged.

They look for shortcuts.

Neither of those paths tends to lead anywhere helpful.

We’re completely agnostic when it comes to money and plans. We work with portfolios ranging from under £100,000 to over £10 million. Having less - or more - doesn’t exclude anyone from sensible, common-sense pension planning.

Buy low, sell high and expect the markets to cycle up and down. Many people have difficulty in regulating their financial emotions when market volatility is emblazoned across all the media, but you know the markets simply turn round and climb back up. If they don’t, that’s not problem either, as that would simply be a permanent devaluation affecting everyone and everything, so be patient.

“The dividend income we run comes from the shares themselves, not from the value of those shares – so don’t sell them.”

Wherever you are today, that’s the right place to begin, it’s easier to live in the present if you have the next twenty years figured out. Planning ahead, and talking about it, is just what you’d tell the kids to do.

If you’d like to have a relaxed, judgement-free conversation about your pension and what’s possible from here, we’d always be delighted to help.

Don’t take short cuts; at your age, this is not the time to gamble pension capital. Patience is your friend, the markets will recover from any downturn.

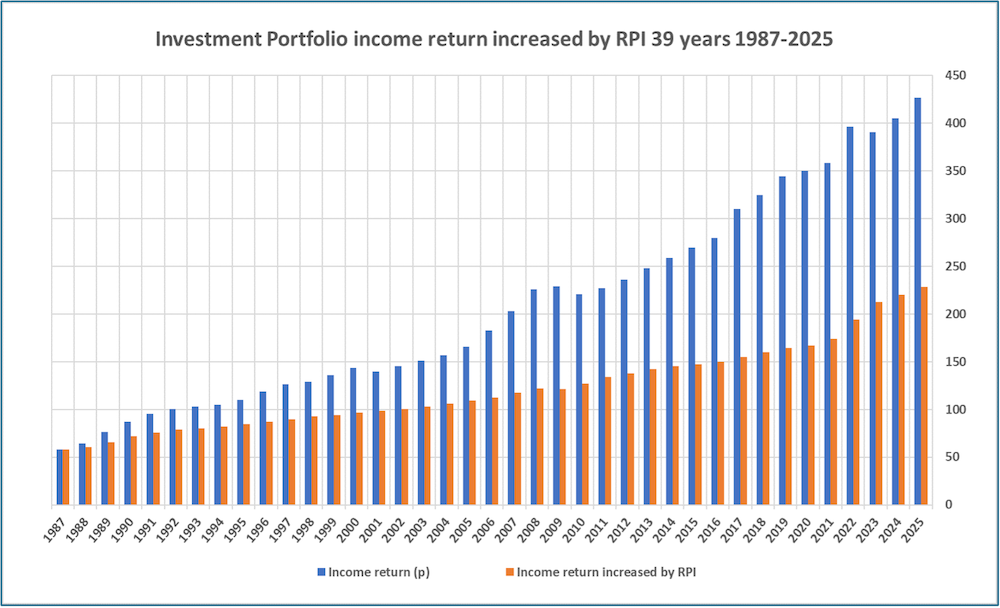

/2. How the portfolio incomes have measured up against inflation.

We take the hard path by using RPI, not CPI.

You’ll be retired for a long time so it’s important to remember that when we were teenagers a pint of Double Diamond or Trophy bitter was around 32p, compared to today’s £5-6. Inflation happens, you might not be buying so much beer in your 80’s but you won’t want to be worrying about your energy bills or food costs.

We measure dividend increases and RPI on a five-year rolling basis rather than discrete years. This way you avoid trying to force your portfolio to generate the 11% increase in RPI that we saw in 2022 – if you do want inflation guarantees, you’ll need to use index-linked gilts, and they are such poor value to the retail investor today.

Our tracking is calculated this way: we pick a start year and identify the dividend income for that year. That same dividend we then increase by RPI every year thereafter. For comparison, we plot beside that the actual dividend that just happened to be paid, so see how it keeps pace with RPI - or not.

This is why we choose trusts’ dividend income over fixed interest. Job done.

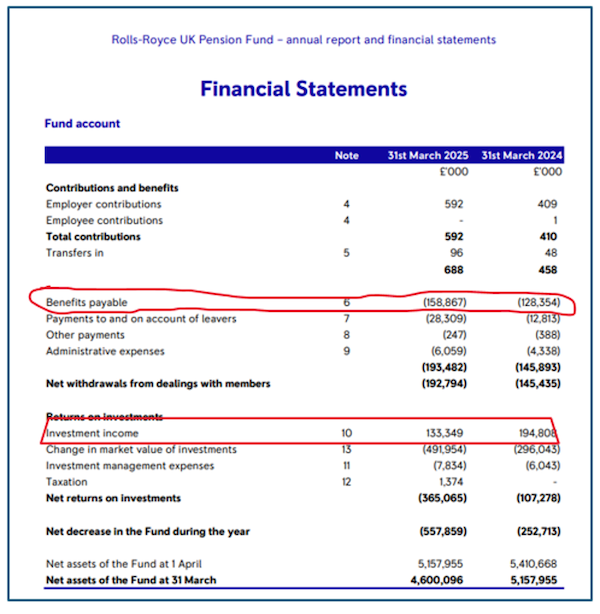

/3. The insides of the Rolls Royce final salary pension engine.

This is the inside of the Rolls Royce F130 engine:

This is the inside of the Rolls Royce defined benefits scheme:

The scheme generates cash income and receives cash premiums to payout its cash benefits. The value of the capital in both these years fell, the income paid out increased because it is not correlated to the capital.

We’re not the clever people, we just copy what the clever people do and it’s worked out for our clients since we started working this way. Simples.

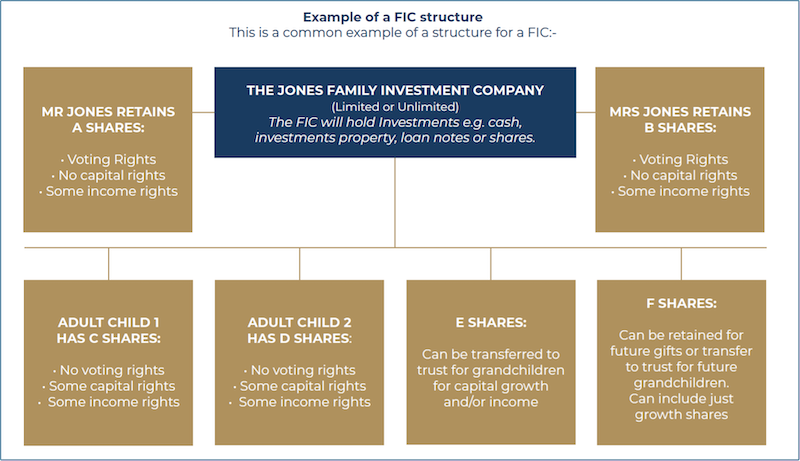

/4. A Family Investment Company: what is it, and should you?

Probably not, however, you’ll hear this IHT shelter bandied about in the media so with thanks to our chums at Rathbones, we thought you’d appreciate a summary of the ‘what and why’.

“It’s not about tax; it’s about control and continuity.”

If you spend any time around ultra-high-net-worth families, you’ll hear the phrase Family Investment Company cropping up more and more.

An FIC is, at its simplest, a private company set up to hold and grow family wealth. Instead of owning investments personally, the family owns shares in the company - and the company owns the assets. What makes it powerful is the flexibility. You can separate control from benefit. Mum and Dad (or grandparents) might hold voting shares and steer the ship, while children hold non-voting shares and participate in the growth without having their hands on the wheel.

In other words: you can support the next generation without handing over the keys on day one.

Who are they for?

FICs tend to suit families who are thinking long term - multi-generational rather than just “this tax year”.

They’re usually appropriate where there are significant assets to invest. Setting up and running a company properly requires legal and tax advice, ongoing filings and governance. That means cost and complexity, so this isn’t a structure for modest estates.

They work well for families who:

Want to pass wealth down gradually and thoughtfully

Value control and clear decision-making

Prefer a more corporate, disciplined framework

Are comfortable with board meetings, documentation and formality

For some families, that structure is a burden. For others, it’s exactly what keeps everyone aligned.

Why are they seen as tax efficient?

Tax is never the only reason to do anything - but it matters.

Broadly speaking, investments within an FIC are subject to corporation tax rather than personal income tax or capital gains tax. UK dividends received by the company are usually exempt from corporation tax, meaning income can roll up within the company and compound over time.

Crucially, shareholders are generally taxed personally only when money is extracted - for example, via dividends. That gives families control over when and how funds are taken. Shares can also be gifted over time as part of estate planning, separating ownership from control. Some FICs are funded via loans from founders, allowing capital to be repaid in a tax-efficient way - though this needs careful structuring.

The detail matters enormously, and tax advice is essential. But used correctly, the structure can be efficient.

The advantages

Done well, an FIC can offer:

Long-term control for senior family members

Centralised investment management across portfolios, property and cash

Flexible ownership, separating voting and economic rights

Clear governance, reducing misunderstandings

Potential tax efficiency compared to personal investing

It can sit neatly between outright personal ownership and a traditional trust.

And the drawbacks?

They are not a magic wand.

There are setup and running costs. There is administrative responsibility. There are compliance requirements. And for smaller estates, simpler structures are often more sensible and cost effective.

It’s also worth saying that FICs are not necessarily a replacement for trusts. Trusts remain hugely valuable in many scenarios, particularly where legal separation of assets is required. In fact, trusts and FICs can work very well together.

The bigger picture

At heart, this isn’t about tax. It’s about control, clarity and continuity.

Families want confidence that their wealth will be managed well - not just for them, but for children and grandchildren. An FIC can provide a disciplined, long-term framework for doing exactly that. But the structure should always follow the strategy, not the other way round.

The right starting point isn’t “Should I have a Family Investment Company?” It’s: What are we trying to achieve as a family?

From there, the appropriate structure usually becomes clear.

About the author

Doug is the Founder and CEO of Chancery Lane. He has worked with personal investing since 1989, specialising in income investing for the last fifteen years, firstly with Old Mutual and running his own award winning business since 1995. Doug is chartered with two professional institutes, CISI and CII and holds the Certified Financial Planner licence.