Of fur coats and knickers...

by Doug Brodie

/1. Going broke slowly.

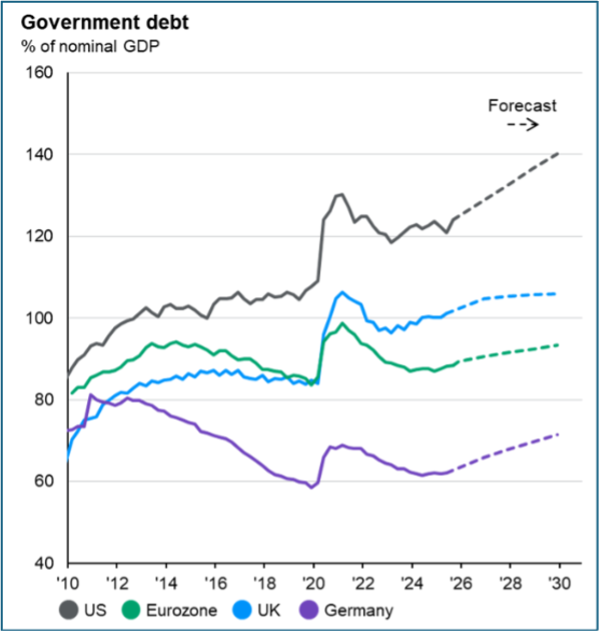

‘Going broke slowly’ is a strapline of the current view of a senior JP Morgan economist (I added the fur coat analogy). Just as you’ll have known neighbours, friends or family who have gone into hock to put a shiny new house or toy into their lives, so America is doing the same. The difference, of course, is that unlike Wayne next door with his leased BMW, America can print its own money to pay off its own debt.

The trend is not good; for once, we (the UK) seem to be the sensible cousin regarding government debt, however, to mere mortals like you and me, this amount of debt is always slightly disconcerting: we hope they know what they’re doing.

Source: JP Morgan

By the time you’ve reached the age where you’re interested enough in what we do that you’ve subscribed to our blog, you’ve learned that ignoring ‘red letters’ is not a good strategy. Someone needs to tell that to our American chums. At what level of debt does this fall over?

Several years ago I met with a teacher who was at the top of his profession; being in the final salary Teachers Pension Scheme is great, however, there’s a price to pay. If the annual increase in the future pension is above the set limits (£60k), then there’s a tax to pay. This person was in their 40’s so any post received from the pension scheme was just ignored – well, not going to retire for ages, so why bother? By the time we got involved and ran the accumulated tax bills, the tax owed had climbed to circa £140,000, more than a year’s salary. Like the US government, you can’t ignore debts forever, one day there will be a reckoning. (*He thought he’d have to sell his house, we managed to get the scheme to pay it for him).

/2. Equities & bonds: how to lose your shirt on bonds and gilts.

Equities are shares in a company; bonds are loans taken out by companies or governments. Both equities and bonds are sliced up into miniature sums so you and I can buy them. For example, HSBC is worth £236 billion for the whole lot, however, you can buy just one share of it for £13.76. With bonds, the UK government borrowing is called gilts – the 4.45% 2035 gilt is worth £18.35 billion in total, however you can buy just one gilt for £103.

Bonds are loans made to the issuer so if you buy a gilt, you are quite simply lending money to the UK government, and they have to repay you. The gilt pays a fixed interest sum every six months and pays the capital back on a fixed date (on the case above it’s 22nd October 2025). The bond is contractual – there is a clear legal obligation for you to be paid, which is why bonds are always seen by ‘the Industry’ as less risky than shares.

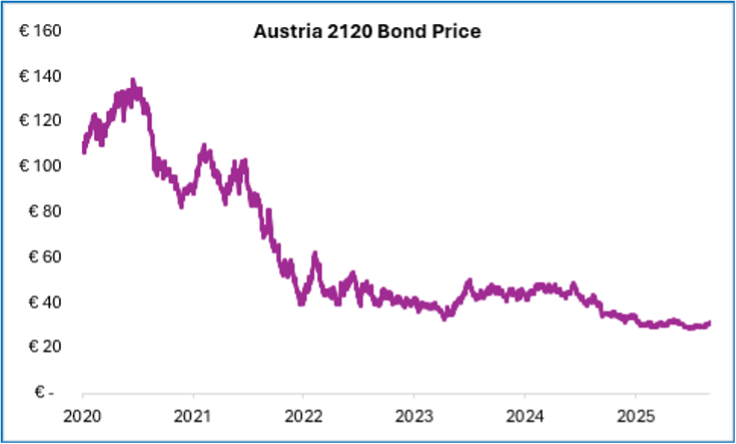

But – take a look at the reality in this chart. In 2020 Austria went to investors and said it wanted to borrow €2 billion for 100 years (not a typo – it will repay in 2120). The investors actually offered to buy almost €18 billion of that money, effectively offering to lend Austria, the country, all that money not to be repaid for 100 years. The chart below shows what has happened to the price of that bond since; someone is holding a bunch of Austrian I.O.U. debt that is seriously under water. However, if the money is genuinely to be parked out for 100 years, the only people actually losing money are those who have changed their minds and actually have to sell now. Time is the risk – as long as you hold for the whole 100 years, as the Austrians said at outset, you won’t lose any money: they guarantee it. The risk to the investor is if they get their timing wrong and have to sell the bond in the (second hand) market.

So no, bonds are not risk-free, far from it.

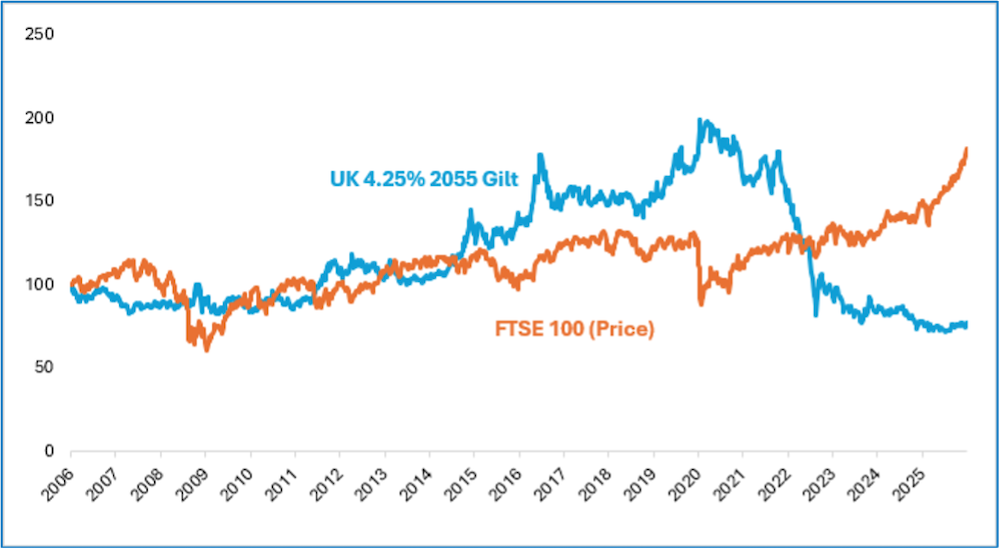

And to avoid anyone thinking I’m being unfair to Austria, or cherry picking a one-off example, here is the 30-year UK gilt charted against the FTSE – which one do you think has the higher price volatility?

/3. The market correction: the timing and the size are all that’s missing.

…and how to ensure your income doesn’t follow the markets down the cliff

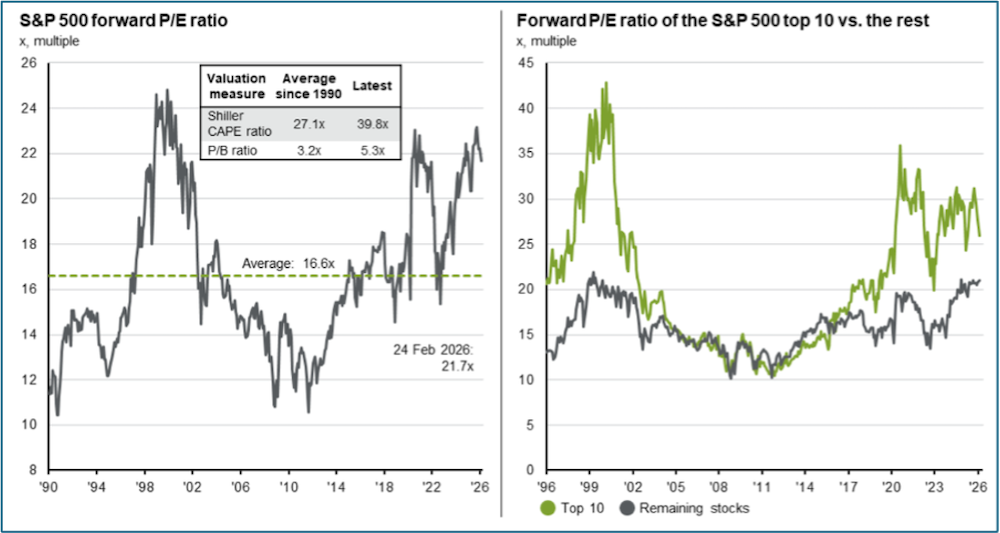

Over last 40 years the S&P has delivered 12% per year. That is due in part because in 2023 it rose 26%, 2024 it rose 25% and in 2025 it was 18%. Before anyone gets excited, it happened to lose -18% in 2022, so it’s not just one-way traffic, and it’s not easy money every year. The charts above show relative valuations – you don’t need to get technical in understanding the numbers, it simply says that compared to the average valuation since 1990, the American market is 30% more expensive today. The chart on the right simply points out that the 10 largest companies in the S&P index are 25% more expensive than the rest.

The market will correct, we could easily see a fall of 20%, or more, or less, but we have no idea when. Markets ‘revert to mean’, in that values go above and below their long-term averages, and everything is cyclical. When we, you, they talk about the ‘market’ falling, we mean the value of the shares, that is, the capital value.

“Do not forget that when the S&P 500 peaked in March 2000, it then took 7 years for it to get back to that value.”

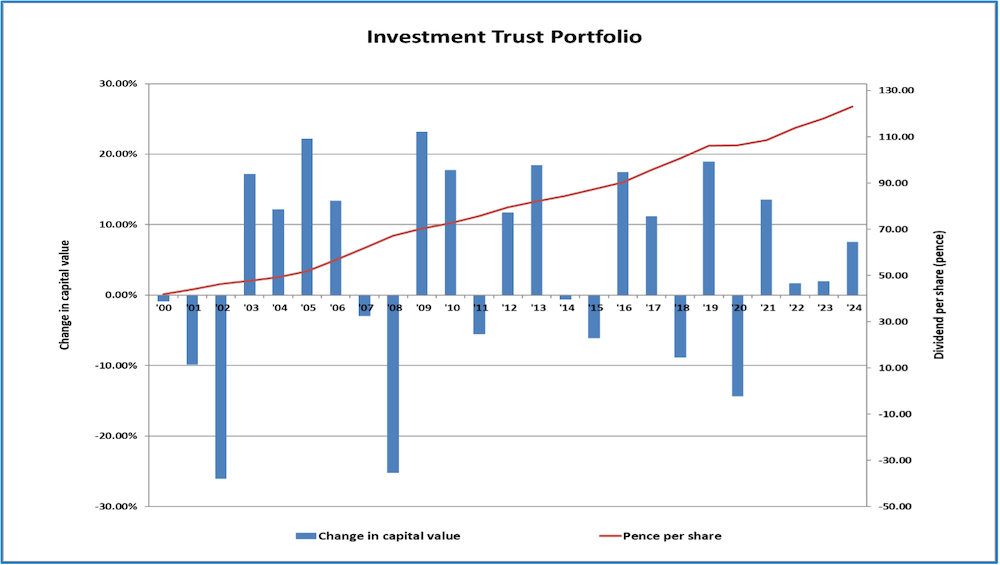

We were running client money back then, as we were through 2007/08 and all subsequent corrections; your Chancery Lane portfolios are designed to ignore those market corrections and deliver your income come what may.

A personal note here, I had previously followed the industry’s mantra of asset allocation, stocks & bonds, 60/40, ‘time in the market’ etc as I had been taught, however, sitting in 2000 watching client values head south gave me the kick to find out how final salary schemes managed to provide income come what may. This is how we now design our client portfolios. We do not blindly follow institutional textbooks for funds.

This is what happens to client income with our strategy: the red line is the income, the blue bars are the capital – the two are not correlated. The income of any portfolio we run has never failed to increase in any year – not guaranteed to do so, however, that is the current record.

/4. Ok, so you want to do Bitcoin – try doing it without falling for The Winner’s Curse…

Richard Thaler is an economist who won the Nobel Prize; oddly, he chose the hard way round. You and I think of economics as maths and graphs and charts and guesstimates, however the chummy Mr Thaler took the view that human interaction is a key factor in financial outcomes, and how right he is. (His books are very readable, try some).

His latest book is titled The Winner’s Curse and it starts with that observation. Imagine you have a jar full of coins and you ask ten people to bid for it: Thaler’s research proved that the majority will undervalue the jar because humans are naturally cautious with money, however the winning bid pretty much always overvalues the jar, and overpays.

Oil leases: plots of land in the US are auctioned off for their oil rights, the right to drill and sell oil. Drilling is always blind and you can’t see in advance if or how much oil is actually there in that lease.

Studies of auctions for the leases showed that the winning bids almost always overbid, and the amount of oil recovered was less than expected.

This gave rise to the Winner’s Curse, where the fact of the winning bid is that all the other bidders collectively thought there was less oil than the winning bidder thought – and the group were most frequently correct.

When you buy Bitcoin, you are buying from someone else who sees more value in cash than the value in that Bitcoin. If you buy as a retail investor you simply look at the price on a trading platform and then buy it, however if you are a major investor, then you effectively bid for your large volume. Investment markets work on the premise of ‘Bid and Offer’ – the Bitcoin is offered by the seller, and you bid. When your bid wins, that does not mean you are the only person wanting to buy, it does mean that many, many other buyers did not want to buy at the price you paid, their bids were lower than yours.

So here’s a thing, if you buy ₿itcoin, why did Goldman Sachs, JP Morgan, Merrill Lynch and all the giant hedge funds not snap it up first? Why are they not keeping it all themselves? Do you feel lucky you won the bid? Do ya’?

About the author

Doug is the Founder and CEO of Chancery Lane. He has worked with personal investing since 1989, specialising in income investing for the last fifteen years, firstly with Old Mutual and running his own award winning business since 1995. Doug is chartered with two professional institutes, CISI and CII and holds the Certified Financial Planner licence.