Set phasers to protect

by Doug Brodie

Captain James T. Kirk’s original phaser sold at auction in 2024 for $910,000. Whether it works or not, the new owner declined to comment, however the phaser used in client investing is mathematically designed to work. It simply means that we split the investment sum into multiple purchases over weeks or months, and in this way we guaranteed that the whole investment is not placed at the top of a recent market level.

Investing at one price is gambling that price is right: that’s luck, not strategy and will only be verified in the future months or years. In all cases, we buy at multiple price points for clients – think, for example, of every 15th of the month for four months. The date is irrelevant, it just needs to be fixed to ignore anyone ‘taking a view’ or trying to call the market. It’s a very simple, very reliable safety feature.

/1. How not to invest.

Our ‘mentor’ is Charley Ellis, author of Winning the Loser’s Game, ex director of Vanguard and investment chief in various institutions. It is he who taught us to approach investing like tennis, where making fewer unforced errors makes your performance much better.

Don’t try to be smarter than everyone else, just less stupid.

- Charlie Munger

Here are the most common errors we see and read about:

Starting Without a Clear Strategy

Jumping in without defining goals - target income level, investment horizon, whether you need income now or later (accumulation vs drawdown), and your risk tolerance. Without this, portfolio construction becomes reactive rather than purposeful.

Chasing High Yields

This is probably the single most common error. A 9% yield often signals distress - dividend cuts, falling share prices, or unsustainable payout ratios. Many amateurs are drawn to the highest yielding stocks or funds without understanding why the yield is elevated. A solid 4% yield from a growing, well-covered dividend is usually far superior to an unreliable 8%.

Ignoring Dividend Cover and Sustainability

Looking only at historic yield rather than whether the dividend is actually covered by earnings or free cash flow. Payout ratios above 80-90% in cyclical businesses are a red flag. REITs and infrastructure funds have different metrics, which adds another layer of complexity many overlook.

Poor Diversification

Over-concentrating in a handful of UK income stalwarts - Lloyds, Legal & General, housebuilders, FTSE 100 defensives - often clustered in the same sectors (financials, energy, telecoms). A truly diversified income portfolio should span sectors, geographies, and asset classes (equities, bonds, infrastructure, property).

Neglecting Total Return

Focusing purely on income yield while ignoring capital erosion. If a share yields 6% but falls 20% over three years, you've lost money in real terms. Income and capital growth should be considered together.

Ignoring Inflation

Locking into fixed income products (certain bonds, annuities, fixed-rate preference shares) without considering real purchasing power over time. In a 3-4% inflation environment, a static 4% income quickly loses its value. Dividend growth investing addresses this - many overlook it.

ISA and Pension Allowances Not Maximised

Holding income-producing assets outside an ISA or SIPP and paying unnecessary Income Tax on dividends (above the £500 annual dividend allowance) or interest. The sequencing of what you hold where (asset location) can meaningfully improve net returns.

Reinvesting Income Haphazardly

Either withdrawing income unnecessarily during accumulation (losing compounding benefit) or reinvesting into already-overweight positions rather than rebalancing toward underweight areas of the portfolio.

Overreliance on a Single Vehicle

Using only individual shares, or only funds, rather than combining the two appropriately. Investment trusts - often misunderstood - can be particularly powerful for income investors given their ability to smooth dividends from revenue reserves. Many amateurs ignore them entirely.

Timing the Market

Trying to buy income stocks on dips or waiting for the "right time" rather than drip-feeding (pound cost averaging) and letting compounding do the work over time.

Not Reviewing Holdings Regularly

Set-and-forget can work for passive index funds, but active income portfolios need periodic review. Dividend cuts, deteriorating balance sheets, rising debt, or management changes can all undermine income expectations.

/2. How to invest through crashes.

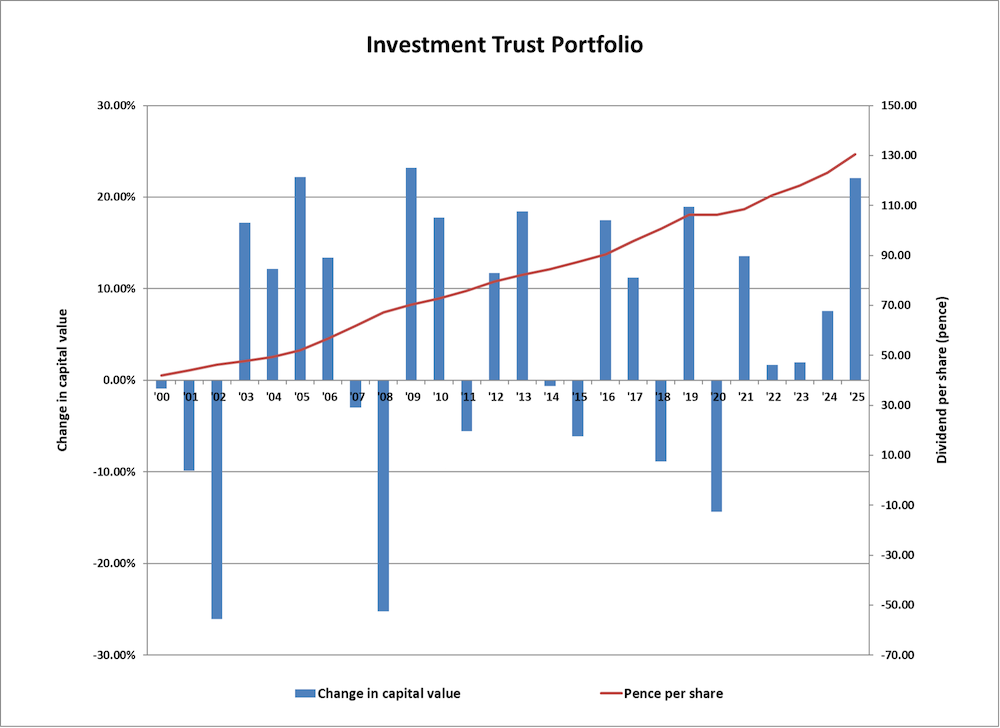

This is the data covering dotcom, GFC, Covid + Ukraine.

This is the key chart, we show it regularly; it’s the single most important investment strategy for drawdown investors to understand. The blue bars are the share capital values, and they rise and fall in line with the market. You can see the value collapsing in 2008, 2011 and 2020. The red line is the income, and it has not fallen once. This is why we invest the way we do. The income is supported by the balance sheet reserves in the trusts, which unit trusts, pension funds and ETFs simply don’t have. It’s not alchemy, it’s not financial engineering, it’s not complicated. Simply holding reserves back means that there is spare money available if needed. It works.

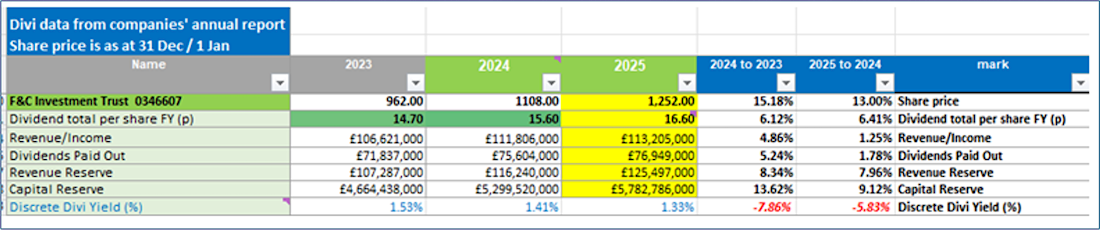

/3. How to read investment trust data: F&C has never missed a dividend since start in 1868.

F&C has just declared its final dividend for 2025, meaning we now know that the full dividend for the 2025 fiscal year was 16.6p per share. It is the very first retail mutual fund, anywhere on the planet. It started investing in 1868 and paid its first dividend in 1869. It has never failed to pay a dividend in any year since. (The Australians popped over for some cricket).

The table above shows its income and its dividends. It shows that the share price increased by 13% from 2024 to 2025, and over 15% in the prior year.

Look at the yield: the two figures in red show that the discrete dividend yield fell in each of the last two years. We already know that the share price had strong growth, however if the dividend failed to match that growth, then the discrete yield will fall. It doesn’t matter, it’s usually a red herring, the yield quoted is only relevant to the investor buying the share today. Yield is the income over the price – and the relevant price is the one you paid, not the one on the market today.

Look at the reserves: the revenue reserves have been steadily growing, and that initially suggests an increasing dividend is being supported by increasing reserves. If we saw the dividend increasing but the reserves falling, that would be a warning bell, and this does indeed happen. Interestingly, the capital reserves could also come into play: in 2012, the law was changed to allow trusts to pay dividends from capital reserves, so with F&C, the annual dividend payment of £76.9 million could actually be paid for the next 76 years from reserves alone.

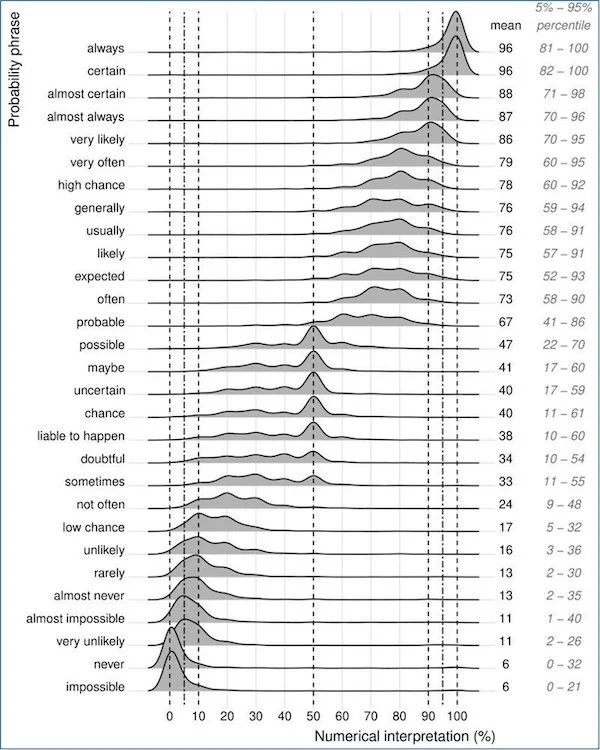

/4. It’s not guaranteed, but does it make it any less likely?

Listening: did you hear what I said, or was it what you heard?

This is the output of a scientific paper on common understanding of different descriptor terms of likelihood; when we say the word ‘probable’, we know what we mean, but do you hear what we mean or is your understanding different?

𝘗𝘪𝘤𝘵𝘶𝘳𝘦 𝘤𝘳𝘦𝘥𝘪𝘵 𝘢𝘯𝘥 𝘰𝘳𝘪𝘨𝘪𝘯𝘢𝘭 𝘱𝘢𝘱𝘦𝘳: Willems, S., Albers, C. and Smeets, I. (2020). Variability in the interpretation of probability phrases used in Dutch news articles - a risk for miscommunication JCOM 19(02), A03.

As is the case, I know what I said, but I can’t know what you think you heard. We have a saying in the office:

“I can explain it to you, but I can’t understand it for you.”

About the author

Doug is the Founder and CEO of Chancery Lane. He has worked with personal investing since 1989, specialising in income investing for the last fifteen years, firstly with Old Mutual and running his own award winning business since 1995. Doug is chartered with two professional institutes, CISI and CII and holds the Certified Financial Planner licence.