Inflation time for llamas.

by Doug Brodie

In this blog:

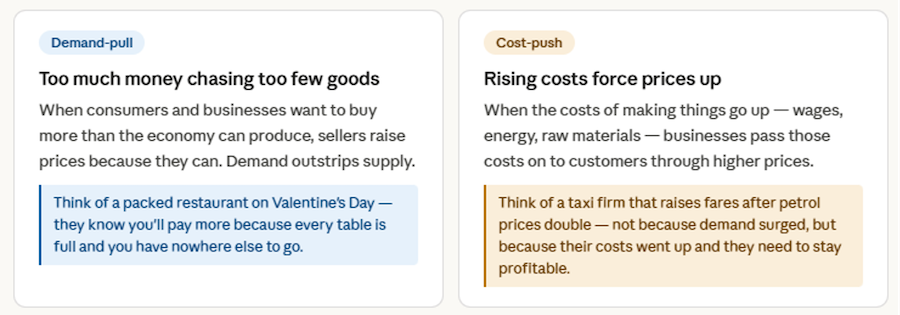

/1. Inflation is created in two ways: a demand-pull on prices, and a cost-push.

/2. It’s not an investment; it’s an M&S investment.

/3. Duration: what it is, what it’s not, do NOT invest in bonds or gilts without knowing.

/4. Winner takes all: why women are the ultimate controllers of personal wealth.

/1. Inflation is created in two ways: a demand-pull on prices, and a cost-push.

| Demand-pull | Cost-push | |

|---|---|---|

| What drives it | Strong consumer spending, low interest rates, government stimulus, high employment | Rising energy prices, supply chain disruption, wage increases, raw material shortages |

| Effect on output | Economy is usually growing - GDP rises alongside prices | Economy can stagnate - prices rise but output may fall (stagflation) |

| UK example | Post-pandemic 2021 spending boom as lockdowns lifted and savings were released | 2022–23 energy crisis after Russia's invasion of Ukraine pushed gas and electricity bills sharply higher |

| Bank of England response | Raise interest rates to dampen borrowing and spending - a relatively clear tool | Rate rises are less effective; can't fix a supply problem by cooling demand alone |

| Who tends to benefit | Workers (jobs plentiful) and some asset owners; debtors repay in cheaper pounds | Energy and commodity producers; no broad group benefits - most people are squeezed |

| Where it shows first | Services, leisure, hospitality - sectors where consumer demand is strongest | Utilities, transport, food - sectors closest to raw material and energy costs |

The current pressure is ‘cost-push’, a key reason why the Bank should not attempt to use interest rates to cool it – it’s not people spending ‘easy money’, it’s the Middle East and oil again. A few things worth noting that aren't obvious from the table:

In practice, the two types often overlap. The 2022–23 UK inflation episode was primarily cost-push (energy and food), but the tight labour market and post-Covid spending also added a demand-pull element on top - which is part of why the Bank of England's rate rises were controversial. Critics argued you can't solve a gas supply crisis with higher mortgage rates.

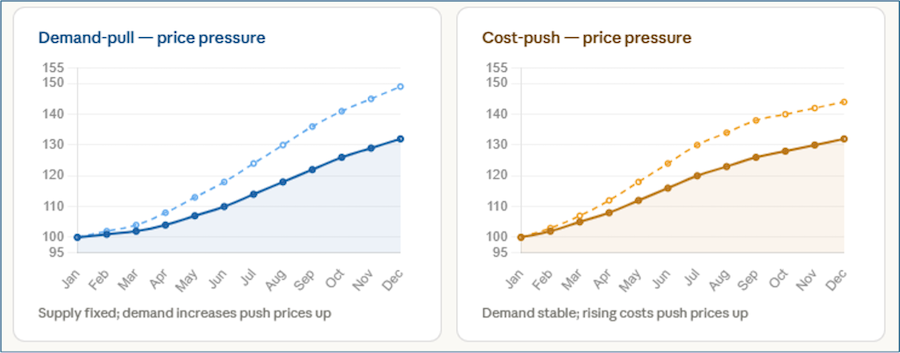

The charts use the same price scale, so you can see that both types can produce similar-looking inflation numbers - but the underlying causes and the right policy response are quite different. Cost-push is the harder one for central banks because rate rises are a blunt instrument aimed at demand, not supply.

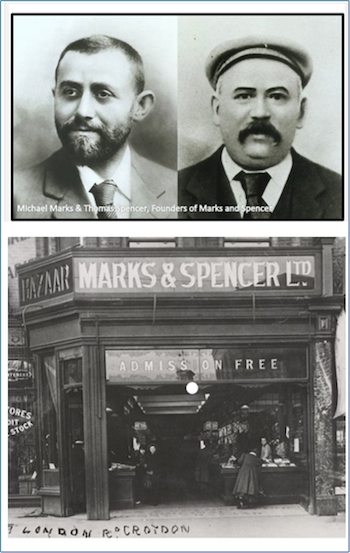

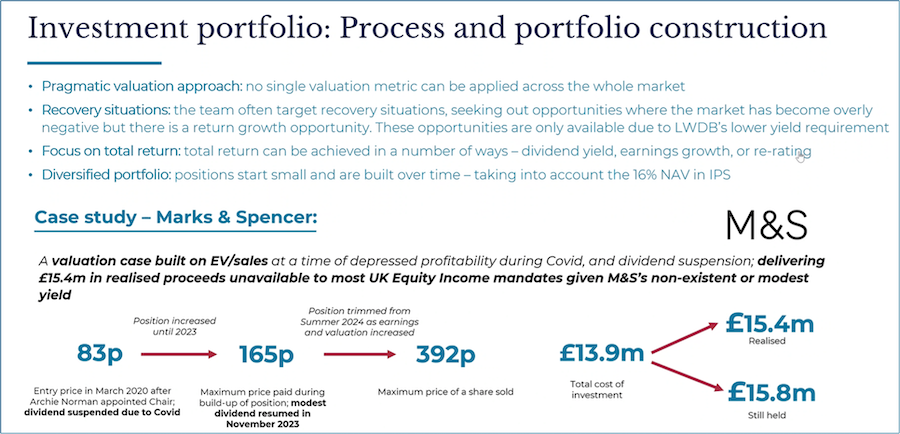

/2. It’s not an investment; it’s an M&S investment.

Income realised + value still held.

We like Law Debenture, a lot. They have just released their latest financial report and update (dividend up 6%), and they outlined their investment in Marks & Spencer. They started to invest in 2020 specifically because Archie Norman was appointed chairman. This is how an investment manager invests; they buy at different stages and sell / trim at different times. The end result is that they invested £13.9m, have sold and pocketed £15.4m and they are still holding shares worth £15.8m. Great strategy, great example.

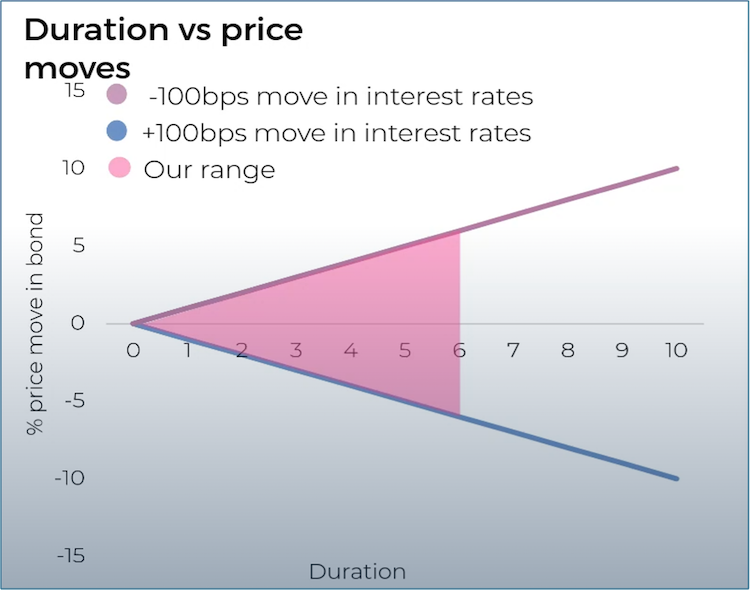

/3. Duration: what it is, what it’s not, do NOT invest in bonds or gilts without knowing.

Duration, in plain terms, is a measure of how sensitive a bond (or bond fund) is to changes in interest rates.

The number itself is expressed in years, but it's easier to think of it as a rule of thumb: for every 1% rise in interest rates, the price of the bond or fund will fall by roughly that many percent - and vice versa.

A simple example:

A bond fund with a duration of 5 years will lose roughly 5% of its value if interest rates rise by 1%.

If rates fall by 1%, it will gain roughly 5%.

Why does duration vary?

Two things push duration up or down:

Time to maturity - a bond that matures in 20 years has much more of its value tied to distant future cash flows, making it far more exposed to rate changes than one maturing in 2 years.

Coupon size - a bond paying a high regular coupon returns cash to you sooner, so less of your money is "at risk" for as long. A low-coupon or zero-coupon bond has a higher duration for the same maturity.

The practical takeaway is that when interest rates are expected to rise, you generally want lower duration - less sensitivity, less price risk. When rates are expected to fall, higher duration bonds and funds benefit more from the price appreciation.

/4. Winner takes all: why women are the ultimate controllers of personal wealth.

The Changing Face of Wealth: What the Industry Needs to Consider

A significant demographic shift is underway

Over the coming decade, the balance of wealth ownership in the UK and across Western economies is expected to shift materially. Longer female life expectancy, evolving inheritance patterns, and rising female earnings are combining to transfer a growing proportion of accumulated wealth into women's hands. For the wealth management industry, this represents both a challenge and an opportunity.

The challenge is that an industry largely built around one client profile may need to broaden its thinking. The opportunity is that advisers willing to do so early will be better placed to serve the clients of the next generation.

Different priorities, not different ambitions

It would be a mistake to assume that wealth simply changes hands without changing character. There is a reasonable body of research suggesting that women, on average, approach financial decisions with a somewhat different set of priorities - though it is important not to overstate or oversimplify this.

What the research broadly points to is a relative emphasis on long-term security, flexibility, and purposeful use of capital - alongside financial return. ESG and impact-oriented investing, charitable giving, and family wellbeing tend to feature more prominently as considerations. This does not imply lesser financial ambition. It suggests that wealth may be expected to serve a wider range of goals.

Advisers who frame their proposition purely around accumulation and asset growth may find that framing is less resonant with a growing segment of their client base.

Evolving patterns of inheritance and distribution

Demographic trends add further complexity. Fertility rates in the UK have fallen to historically low levels, and a rising proportion of women are reaching later life without direct descendants. The traditional assumption - that wealth passes predictably between spouses and down to children - is becoming less reliable as a planning framework.

Where direct heirs are absent, wealth tends to flow more broadly: to extended family, friends, charitable causes, and community initiatives. This has practical implications for estate planning, tax structuring, and the legal frameworks that govern wealth transfer, many of which were designed with nuclear family structures in mind.

Later-life living arrangements may also change

There is early but notable evidence of older women - particularly those living alone - exploring more collaborative living arrangements: shared homes, co-housing models, and communities organised around social connection rather than conventional household structures. If wealth increasingly sits with women who are single in later life, demand for financial planning that supports these models may grow.

Implications for the industry

None of these calls for sweeping generalisations about how any individual client thinks or behaves. It does, however, suggest that the industry would benefit from reviewing some long-standing assumptions - about what clients want wealth to do, how it will be passed on, and what good financial planning actually looks like across a longer and more varied life course.

The firms best positioned for the next decade will be those that approach this shift with genuine curiosity rather than simply mapping new clients onto old models.

/5. The Big 5 Retirement Risks: and how to mitigate them.

Here are the five big retirement income risks, explained plainly, with practical ways to reduce each.

1. Outliving your assets (longevity risk)

What it is: Simply running out of money before you run out of life. People routinely underestimate how long retirement lasts. A healthy 65-year-old in the UK today has a reasonable chance of living into their late 80s or beyond - that's potentially 25+ years of drawdown.

How to mitigate it:

Don't plan to an average life expectancy - plan to an older age (90 or 95) to be safe

Keep some guaranteed income for life - the State Pension is the foundation; an annuity (or partial annuity) on top removes the risk of outliving that portion entirely

Avoid drawing down too fast - a commonly cited safe withdrawal rate is around 3.5–4% of your portfolio per year, though this is a rough guide, not a rule

Stay invested in growth assets for longer - keeping some equity exposure in early retirement helps the pot continue growing

2. Sequence of returns risk

What it is: The order in which investment returns arrive matters enormously in retirement - far more than the average return over time. If markets crash in the first few years of drawdown, you're forced to sell units at depressed prices to fund your income. Those units are gone and can't recover with the market, permanently damaging your pot. Good early returns, conversely, give it a strong foundation. Two people with identical average returns over 20 years can end up with very different outcomes depending on when the bad years hit.

How to mitigate it:

Hold a cash or short-term bond buffer (typically 1–3 years of income needs) so you don't have to sell equities in a downturn - you draw from the buffer while markets recover

Be flexible with spending - if markets fall sharply early on, reduce discretionary spending temporarily

Consider phased annuitisation - converting a portion of the pot to guaranteed income at different ages reduces dependence on market performance

Avoid taking too much risk at the point of retirement - gradually de-risking in the years just before and after you stop working

3. Spending shocks

What it is: Large, unplanned expenses that force you to draw heavily from your pot at the wrong time - exactly the scenario sequence risk makes dangerous. Common culprits: major home repairs, a car, helping adult children, divorce, or most significantly, care costs. In the UK, residential care can easily cost £50,000–£80,000 per year, and the means-testing threshold before you fund it yourself is relatively low.

How to mitigate it:

Maintain an emergency fund separate from your investment portfolio — ideally 6–12 months of expenses in easy-access cash

Keep the family home in good repair before retirement so deferred maintenance doesn't ambush you later

Consider later-life care costs explicitly in your plan - they are a genuine financial risk, not just a personal one

Look at insurance options - critical illness cover, income protection, or long-term care insurance (though the UK market for the latter is limited)

Preserve flexibility - avoid locking away all your assets in illiquid structures

4. Declining cognitive abilities

What it is: As people age, the capacity to manage money, spot scams, negotiate bills, and make sound financial decisions can deteriorate - sometimes gradually, sometimes suddenly. This is one of the most underacknowledged retirement risks. Financial elder abuse and fraud are also far more common than most families realise.

How to mitigate it:

Simplify your finances before you need to - consolidate pensions and accounts, reduce complexity while you're still fully sharp

Set up a Lasting Power of Attorney (LPA) early - this is arguably the single most important financial planning step for later life; it allows a trusted person to manage your affairs if you lose capacity. Doing it while you have full mental capacity is essential - you cannot set one up afterwards

Tell someone you trust where everything is - a trusted family member or adviser should know about accounts, pensions, insurance, and debts

Use a regulated financial adviser for ongoing management - a professional relationship provides a layer of oversight

Be alert to scams - discuss this with family; fraudsters specifically target older people, and pressure tactics or "too good to be true" investment offers are serious red flags

5. Compounding inflation

What it is: Inflation erodes purchasing power steadily over time. At 3% inflation, something costing £1,000 today will cost around £1,800 in 20 years. Fixed income - a pension that doesn't increase, or cash sitting in a low-rate account - quietly loses real value every year. This is particularly damaging in retirement because the spending horizon is long and healthcare and care costs tend to rise faster than general inflation.

How to mitigate it:

Value inflation-linked income highly - the State Pension is triple-locked (rising by the highest of earnings, inflation, or 2.5%), making it exceptionally valuable; defined benefit pensions with inflation linkage are similarly precious

If buying an annuity, consider an inflation-linked version - it pays less initially but protects long-term purchasing power

Keep some equity exposure throughout retirement - equities are an imperfect but real long-term hedge against inflation, as company revenues and dividends tend to rise with prices over time

Don't hold excessive cash long-term - cash savings rarely keep pace with inflation after tax

Review your income and spending in real terms - periodically check whether your income is keeping up with what things actually cost, not just in cash terms

How the risks interact:

These risks don't sit neatly in separate boxes. A market crash (sequence risk) plus a care bill (spending shock) in the same year can devastate a plan that looked perfectly sound on paper. Cognitive decline makes someone more vulnerable to fraud precisely when they may have accumulated the most wealth. Inflation silently makes all the other risks worse over time.

About the author

Doug is the Founder and CEO of Chancery Lane. He has worked with personal investing since 1989, specialising in income investing for the last fifteen years, firstly with Old Mutual and running his own award winning business since 1995. Doug is chartered with two professional institutes, CISI and CII and holds the Certified Financial Planner licence.