“Who I want to be” [it’s your retirement, not theirs.]

by Doug Brodie

/1. That’s who I want to be.

What makes a happy retiree

After more than two decades working with people in and around retirement, I've stopped being surprised by what the answer isn't. It isn't the size of the portfolio. It isn't the second home, the business-class flights, or the kitchen extension. The happiest retirees I know - and I know many - share something quieter than any of that. They made a decision, at some point, about what their retirement was actually for. They got specific. Not "travel more" but "spend three weeks every autumn in the same place we love." Not "see the grandchildren" but Tuesday afternoons, reliably, without cancelling. Specificity, it turns out, is what separates a retirement that feels free from one that just feels empty.

Mental health in retirement

Nobody talks about this enough, and they should. Retirement is one of the most significant identity transitions a person can go through, and the mental health implications are real. Losing the structure of work - the colleagues, the purpose, even the mild annoyance of the commute - leaves a gap that surprises almost everyone. The retirees who navigate it best are those who replace structure deliberately, not accidentally. They join things. They commit to things. They stay curious. They resist the pull toward pure leisure, because pure leisure, it turns out, is exhausting after about a fortnight. A fulfilling retirement isn't a permanent holiday. It's a different kind of meaningful.

A healthy relationship with money

Financial anxiety is one of the most corrosive forces in later life, and its cruelty is that it affects people at every level of wealth. I've met people with substantial assets who lie awake worrying, and people with modest incomes who sleep perfectly well. The difference is almost never the number - it's the certainty. When you know that a reliable income is landing in your account each month, sufficient for your actual life, money quietly moves to the background where it belongs. It stops being a daily preoccupation and becomes, simply, the thing that enables everything else. That shift - from anxiety to ease - is what we're really trying to build.

What a fulfilling life in retirement looks like

It looks different for everyone, which is the point. But there are patterns. The retirees I admire most have kept one foot in the world - volunteering, mentoring, part-time work they actually enjoy. They have close friendships they invest in. They have a physical life, not necessarily ambitious, but consistent. They have things they're still learning. And crucially, they have financial breathing room - enough that an unexpected bill, a generous impulse, or a spontaneous trip doesn't require agonising. That combination of purpose, connection, health, and financial calm doesn't happen by accident. It's designed. Sometimes the design starts years before retirement. Sometimes it starts the week before. It's never too late to begin.

Let's talk about your income

The woman in the chair with her morning coffee - unhurried, content, entirely herself - is who most of us are trying to become. She got there with a plan, and the foundation of that plan was knowing her income was sorted. Not optimised to the last basis point. Sorted. If you're approaching retirement and you're not yet certain what your monthly income will look like, or you're already in retirement and it doesn't quite feel right, that's exactly the conversation we're here for. No pressure, no jargon, no agenda beyond helping you build something that lets you get on with your day. We'd love to hear from you.

/2. Total return, capital and income: the data.

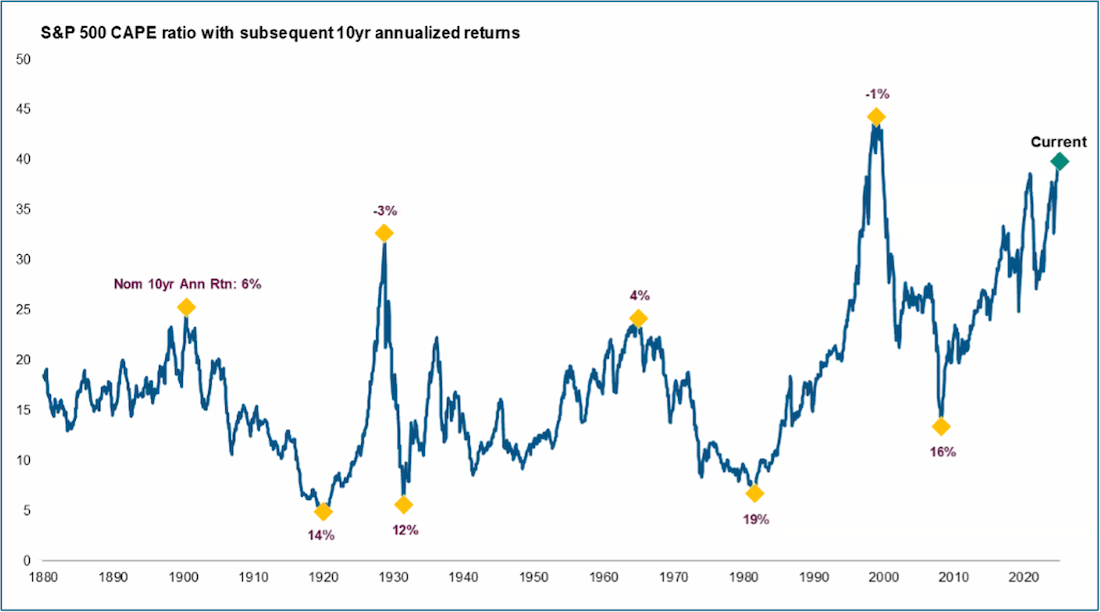

All the information you have is historical, and all the decisions you make are about the future. Spot the mismatch. The chart below shows a blue line representing the relative value of the US market, relative to previous years. For example, you can see that the value now is higher than it was in 1929, but less than in 2000. The yellow diamond figures are the annual returns over the next ten years, starting from that diamond. It shows that from 1929 the return pa was -3% for 10 years, and from 2000 to 2010 it was -1%. In 1965 and 1900 however, the spikes were followed by 4% and 6% annual returns. Your expectation should be that the double digit returns of the past decade are not going to be repeated.

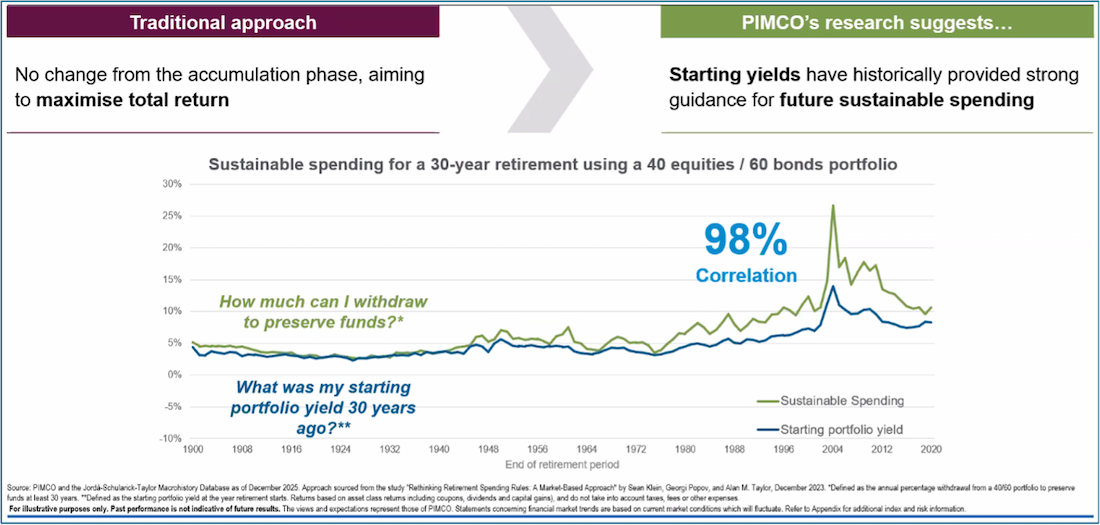

The next chart looks at the correlation between starting income of a portfolio and the chance that income will last for 30 years. What it is showing us is the relationship between the two lines – this means they are indeed correlated, in fact, they are 98% correlated. In layperson’s terms, it means that if your starting yield was, say 5%, then drawing 5% meant your money would not run out. Note: this includes the 1930 depression, two world wars and everything before and after. The message to take is that investment income is a very defensive measure for drawdown.

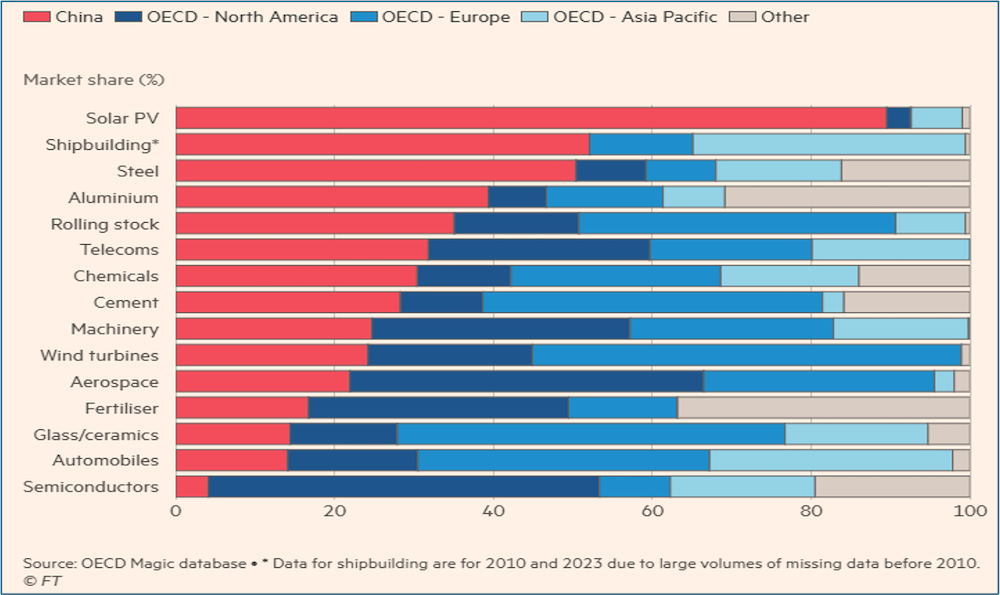

Focusing on income means you can ignore the underlying macro-economic trends, such as this table from the FT showing global market share in various economic sectors:

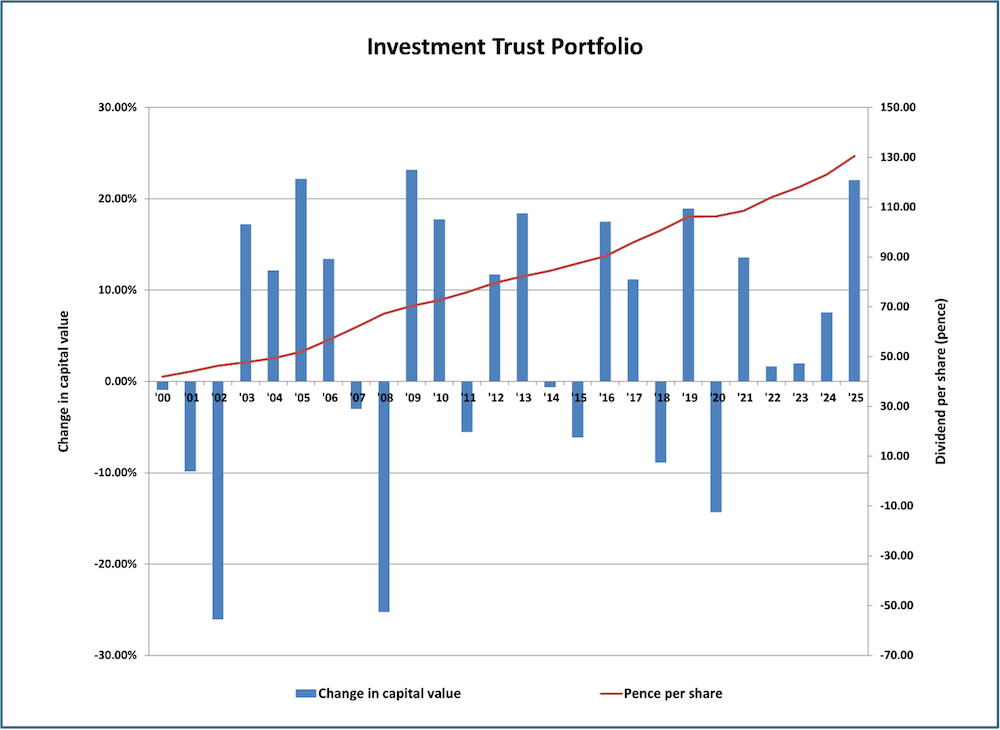

The markets are volatile, so if you are drawing income based on the total return of your portfolio, it too will be wobbly and volatile, changing from month to month. The solution is elegantly demonstrated in our key chart, which shows the annual return of capital in the blue bars, and the annual income in the red line. Which one do you choose for your retirement income?

/3. Do you cycle? Do you train-ish? Alistair Brownlee ring a bell?

Alistair focuses on data science in the field of sports science. In summary, he measures inputs and impacts on physical abilities.

Growing up training on the country lanes of Yorkshire, training wisdom was simple: winter miles make summer smiles. Get your base in, rest when the season ends, build slowly back up.

I still believe in that philosophy. But a dataset of 856,000 activities across 20 European countries gave me a chance to test whether I could find a signal to back this up, and it threw up a finding I didn't expect.

I looked at cyclists who do some level of indoor training through winter, versus those who only ride outdoors. Same summer volume. Same commitment level. The question: does the trainer protect your winter training?

The winter drop was identical. 50% vs 47%. Statistically negligible.

But here's what the data did show. Cyclists who also train indoors ride nearly four times more outdoor hours in winter than those who don't. These motivated individuals are not using the trainer to compensate for lost outdoor riding. The indoor hours supplement the bigger outdoor base that was already there.

- Al Brownlee

In short, he identified that adding the indoor trainer to winter sessions added nothing to cycling competency – the factor that made the difference was getting off your butt and doing something. The message for you and me is that nothing happens unless we make it do so. Your retirement won’t fix itself, however, as long as you are doing the myriad things to ‘exercise’ your retirement, you’ll get the results.

A good retirement is usually not about doing nothing. It is about having enough structure, enough freedom, and enough purpose. Most people do best when retirement has five things in it:

A reason to get up

Work used to provide shape, status, and routine. Retirement needs replacements. That could be volunteering, grandkids, gardening, mentoring, travel, learning, part-time work, or a serious hobby. People tend to struggle when they retire from work but not to something.

A steady rhythm

Not a rigid timetable, but some weekly pattern. A few fixed anchors help a lot: exercise on certain days, lunch with friends, classes, clubs, errands, family time. Too much empty time can feel exciting at first and hollow later.

Movement and health

Retirement goes better when people treat fitness almost like a part-time job. Walking, strength work, balance, sleep, decent food, and routine checkups matter more than lofty plans. Health is what gives freedom meaning.

Real relationships

A lot of retirees underestimate how much work friendships take once the workplace disappears. The happiest retirees usually keep building their social world on purpose, not by accident.

A sense of control

Living within your means, keeping life simple, and avoiding financial anxiety changes everything. Peace often comes less from luxury than from knowing your basics are secure.

A healthy way to think about retirement is:

not permanent holiday

not endless idleness

not clinging to a former identity

but a chance to build a life that is lighter and more chosen

In practice, someone should probably be:

staying physically active

keeping some routine

being useful to other people

protecting their money and health

making time for pleasure without making pleasure their only purpose

continuing to learn and adapt

The people who seem to do retirement best often combine enjoyment, usefulness, and connection. They rest, but they do not drift. A simple test is to ask yourself:

“Does this retirement have joy, structure, and meaning?”

If one of those is missing, that is usually where the discomfort is coming from.

About the author

Doug is the Founder and CEO of Chancery Lane. He has worked with personal investing since 1989, specialising in income investing for the last fifteen years, firstly with Old Mutual and running his own award winning business since 1995. Doug is chartered with two professional institutes, CISI and CII and holds the Certified Financial Planner licence.