How to be rational in volatile markets

by Doug Brodie

/1. How to be rational in volatile markets

It will rebound from the current value; it’s important to remember that if the estate agent tells you your house value has fallen, the God of Property is not picking on you (that would be very mean), which means the house you would be buying will also be correspondingly cheaper. When you read/see the headline of a market fall that affects everyone, it’s not just you, so don’t feel paranoid, and don’t try and fight the tide.

Regular readers know we offer two things: empathy and expertise.

Here’s the expertise part:

Here’s the empathy part:

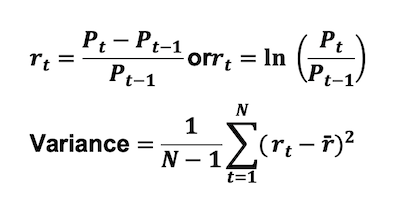

It always feels unnerving, and it happens to everyone, and has done since the start of money, so your reaction to wobbly markets is normal. The formula above is a long-winded way of calculating the daily variance of something, in this case, the capital value of the FTSE 100 index. The daily volatility - every single working day - of the FTSE100 since the US invaded Iran is between 1% and 1.25% per day. The biggest one-day fall was 1.2%, and the largest ‘peak to trough’ was -7.4%.

Our investment trusts pay dividends that are as near as damn it ‘fixed’ – just because it’s not contractually guaranteed does not mean it will not happen – history tells us that. So, if we have £1 of income from an asset, and the price of that asset falls, it just became cheaper per £1 of income, so you can buy more of it.

The share price of Merchants Trust hit £6.56 on 27th February. Its 2025 dividend was 29.2p, so the investor buying it on that day was buying a 4.45% trailing yield.

On 27th March, the share price was trading at £5.76, so those investors were buying the same 29.2p trailing dividend but because they paid less for the same, identical income, their yield was 5.07%.

As the Alliance & Leicester used to tell us, be a smarter investor with the Alli…

The message is, if the market is moving up and down by c1.5% per day, don’t try to time your actions, just phase. You can phase in and phase out, that way you’re guaranteed not to sell out at the bottom. And remember, income and capital are not correlated – you’re getting to see the whole point of income investing played out in front of you. You’re not a hedge fund trader, you probably don’t do this professionally, you probably don’t have the software to see the volume of trades being cleared, being bid or being queued, and for the amount of money you have, the differences are highly unlikely to have any visible impact on your retirement lifestyle.

And the other point to understand from “the market is moving up and down by c1.5% per day” is that the whole year’s charge on your pension is often wiped out just by the luck of the day you invest. Low costs don’t make you money in your investments: when did you ever read about the management charges in Warren Buffett’s company?

/2. The client’s question: the maths of the value of planning your income.

The full state pension is now £12,548 per year and the tax-free personal allowance is £12,570, so any income above that is all taxable. If your total income is £100k+, tax gets troubling:

Q: Alongside the full state pension, how much dividend income do I need to have £7,500 per month after tax?

Full new state pension: £241.30/week = £12,548/year (£1,046/month)

Personal allowance: £12,570 (but see below - it's fully withdrawn at this income level)

Dividend allowance: £500 at 0%

Dividend tax rates (increased from April 2026): 10.75% basic, 35.75% higher, 39.35% additional rate

The answer: you need approximately £9,559/month (£114,700/year) in gross dividends.

Here's why, factoring in the important sting in the tail - the personal allowance trap. Your state pension of £12,548 almost exactly uses up the £12,570 personal allowance so on its own it's essentially tax-free. But once your total income (state pension + dividends) exceeds £100,000, the personal allowance starts being tapered away at £1 for every £2 of income above £100,000. To reach the net income you need, your total income will be around £127,250, which is above £125,140 - the point where the personal allowance disappears entirely. This means your state pension becomes fully taxable at 20%.

Income tax breakdown at £114,700 dividends:

State pension (no personal allowance left): £12,548 × 20% = £2,510

Dividends of £114,700:

£500 at 0% (dividend allowance) = £0

£24,652 at 10.75% (basic rate band remaining after state pension) = £2,650

£87,440 at 35.75% (higher rate) = £31,260

£2,108 at 39.35% (additional rate on total income above £125,140) = £830

Total tax = £37,250 pa

Net income: £127,248 income less £37,250 tax = £90,000 pa or £7,500 pm.

Note: in scenarios like this, holding dividend assets within a bond can easily defer the tax position on some or all of the taxable income.

/3. Law Debenture or Claverhouse – AI for analysis, only when you know the question.

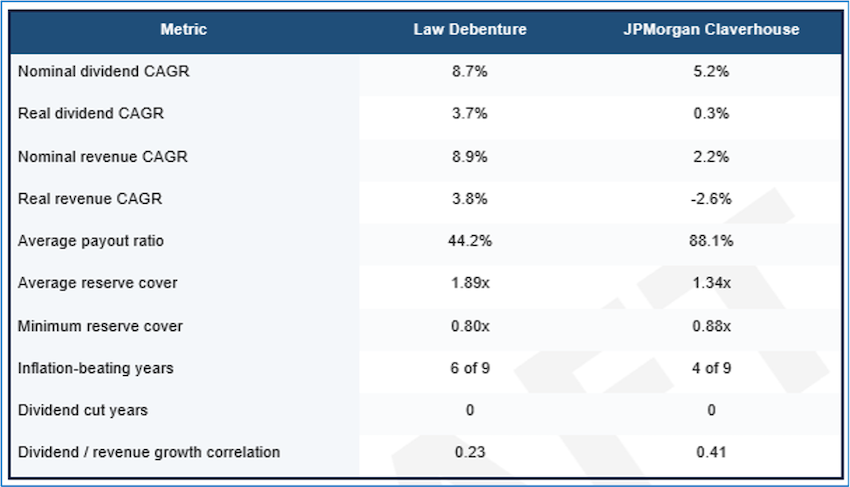

To be in our analysis pool, an investment trust already has to have very strong, robust and reliable financials, dividends and investment criteria; within that pool of 30 or so, we then run a lot of comparisons through the year to work out when one becomes an outlier, what expectations we should have across all the trusts, and which ones we might favour within a portfolio. In general, our portfolios run between 8 and 18 trusts, and some larger client holdings in one trust can nudge £500,000, so we need to ensure that we are as knowledgeable as we can be. This is a summary where we have been analysing the likely dividend payments in future years from JP Morgan Claverhouse and Law Debenture. It starts with manually creating a workbook from the records in Companies House, and extrapolating that data from 1986 forward.

The dataset is the Trust Master Data workbook with revisions up to 12th March 2026. The analysis uses ordinary dividend/share rather than total dividends, so that special dividends do not distort trend comparison. Revenue and reserve variables are taken directly from the panel extracted in the earlier workbook build. RPI is applied to deflate both dividends and revenue when real growth is reported.

Sample period: 2016-2025 for dividends. JP Morgan Claverhouse revenue and reserve fields are available through 2024 only in the source workbook.

Rolling diagnostics: six 5-year windows from 2016-2020 through 2021-2025.

Real CAGR formula: ((end / start) / cumulative inflation)^(1 / n) - 1, where cumulative inflation is the applied product of annual RPI terms inside the window.

Correlation statistic: Pearson correlation between annual dividend growth and annual revenue growth over overlapping years.

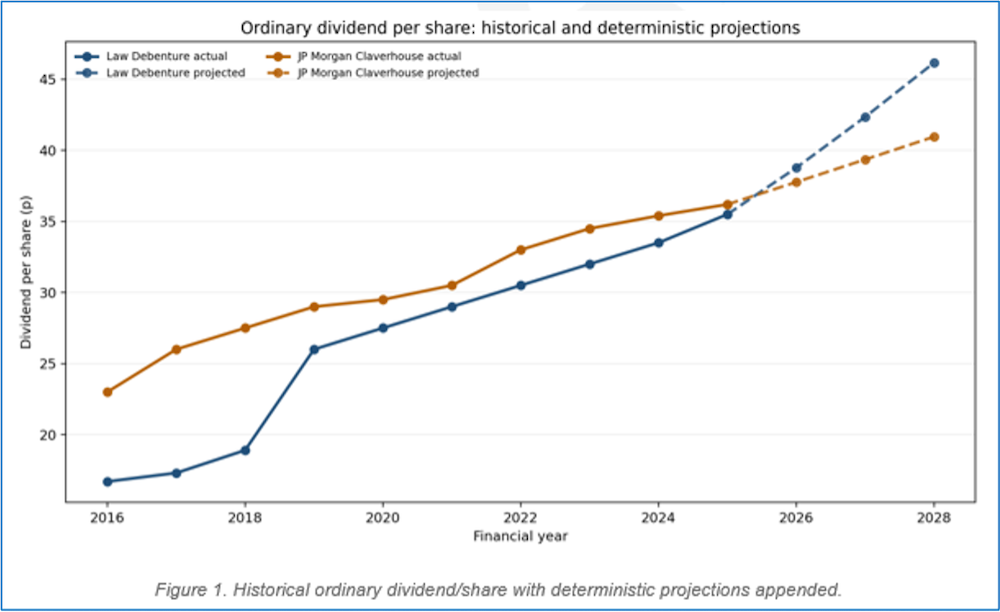

Deterministic forecast equations

Trend div = 0.65 x long-run dividend CAGR + 0.35 x recent rolling-window dividend CAGR

Trend rev = 0.65 x long-run revenue CAGR + 0.35 x recent rolling-window revenue CAGR

Buffer = 1.5% x clamp (recent reserve cover - 1, -1, 2) + 2.0% x clamp (1 - recent payout ratio, -0.5, 0.5)

Penalty = 0.75% x min (dividend cuts in latest 5-year window, 3) + 50% x max (recent dividend growth volatility - 8%, 0)

Growth 2026e = clamp (0.55 x Trend Div + 0.45 x (Trend_rev + Buffer) - Penalty, -5%, 12%)

Growth 2027e = clamp (0.85 x Growth_2026e + 0.15 x Trend_rev, -4%, 10%)

Growth 2028e = clamp (0.70 x Growth_2026e + 0.30 x Trend_rev, -3%, 9%)

Law Debenture generated the stronger long-run income profile.

Which leads to:

Two qualitative features matter. First, Law Debenture experienced a step-up in 2019 from 18.9p to 26.0p, which permanently lifted its dividend base and explains much of the full-period CAGR advantage. Second, JP Morgan Claverhouse has shown steadier but slower compounding. Its dividend series has no cuts, but its real growth has been close to zero once inflation is applied, especially after 2021. Inflation is important in our portfolios.

The dividends are not guaranteed, and our research doesn’t pretend to be flawless, however it’s important for us to do the grunt work so that our and your expectations are prudent, and income goals are deliverable year after year…

/4. Don’t worry, be happy

Here’s a checklist, a prompt, an idea generator. We’ve been working with people at retirement for over thirty years and with clarity, we can say the biggest issue bar none is not money, it’s the transition from a five day / 8 hour working week to nothing.

Happy Retirement Lifestyle Planner

1. Purpose & Meaning

What gives you a sense of purpose?

Consider volunteering (e.g. charities, NHS, Citizens Advice)

Explore part-time or consultancy work

Join local initiatives (community groups, parish/council activities)

2. Social Connection

People to stay in touch with

Join UK groups such as:

U3A (University of the Third Age) (u3a.org.uk)

Hiking / walking / sailing / painting / guitar-learning clubs

Local volunteering groups

Faith or community organisations (people don’t suddenly find God when they’re older, they suddenly find the need for socialising and being useful)

Schedule regular social time (weekly coffee, pub lunch, calls)

3. Health & Fitness (NHS Focus)

Register with / stay connected to your GP

Book NHS health checks (blood pressure, cholesterol, screenings)

Regular activities:

Walking (parks, National Trust, Ramblers groups)

Swimming (local leisure centre)

Gym / classes

Gardening

Aim for 150 minutes of activity per week – buy a Garmin or smart watch, challenge yourself to regular exercise of any type.

4. Mental Stimulation

Join adult learning (e.g. local colleges, Open University, post grad, teaching)

Attend talks, museums, National Trust sites

Read regularly (library membership)

Puzzles, chess, bridge

5. Routine & Structure

Create a balanced weekly routine:

Morning

Afternoon

Evening

Include: exercise, social time, hobbies, rest

Try a weekly “anchor activity” (e.g. every Tuesday = walking group)

6. Money & Financial Security

Check your State Pension entitlement

Review workplace / private pensions – know your income

Consider drawdown vs annuity strategy

Ensure you are using your ISA allowances

Budget for:

Utilities & council tax

Food & transport

Leisure & holidays

Check eligibility for:

Pension Credit

Winter Fuel Payment

Council tax reduction

7. Home & Lifestyle Choices

Is your current home suitable long-term?

Consider downsizing or relocating

Explore retirement communities if relevant

Plan for:

Maintenance costs

Accessibility (stairs, transport links)

8. Freedom & Fun (UK & Travel)

Bucket list ideas:

UK travel (coast, countryside, heritage sites)

European travel (easy access from UK)

Theatre, sport, cultural events

Plan at least one trip or experience every quarter

9. Giving Back

Ways to contribute

Volunteer options:

Charity shops

Food banks

Schools / mentoring

NHS or care organisations

10. Practical & Legal Planning

Write or update your Will

Set up Lasting Power of Attorney (LPA)

Organise important documents

Review insurance (home, health, life if relevant)

Bonus: 5 Golden Rules for Happy Retirement

Secure your income first (State Pension + reliable sources)

Stay socially active – isolation is a major risk in later life

Use the NHS proactively – prevention matters

Spend on experiences, not just saving

Keep structure in your week – routine creates wellbeing

About the author

Doug is the Founder and CEO of Chancery Lane. He has worked with personal investing since 1989, specialising in income investing for the last fifteen years, firstly with Old Mutual and running his own award winning business since 1995. Doug is chartered with two professional institutes, CISI and CII and holds the Certified Financial Planner licence.