Money – The Danger of Overthinking

by Doug Brodie

/1. Money – The Danger of Overthinking

People frequently retire without planning how to fill their time next week; they tend to take an immediate holiday or travelling break, however, shortly afterwards they are back at home, in the middle of a working year, realising that’s Woman’s Hour playing on the radio this rainy Tuesday morning. Boredom sets in, so let’s go through all the money for the nth time, and so starts the fiddling of the pension, reading the slop on the internet:

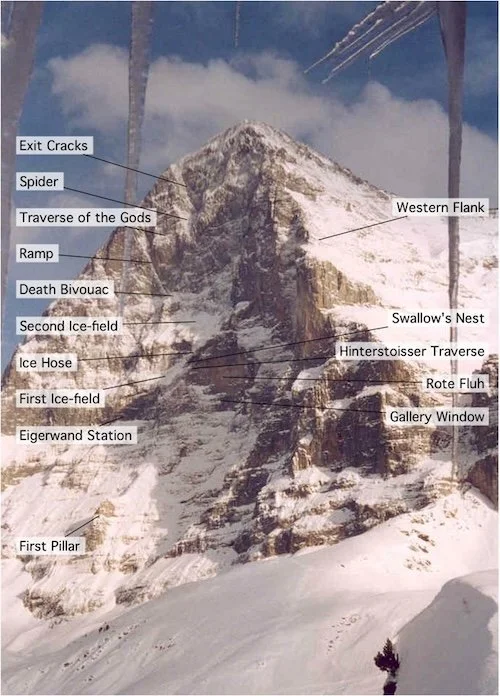

In 1938 Anderl Heckmair led three other climbers to conquer the north face of the Eiger for the very first time. Heinrich Harrer, one of the four climbers, wrote the detailed story in his book The White Spider (I recommend it). It took them three days to climb from top to bottom, sleeping tied onto the rock face as they went. Three years earlier, Mehringer and Sedlmeyer had tried and failed to be the first, the two of them freezing to death while ‘camped’ on the rock face at 3,300 meters. Three days is a long time on a frozen rock face.

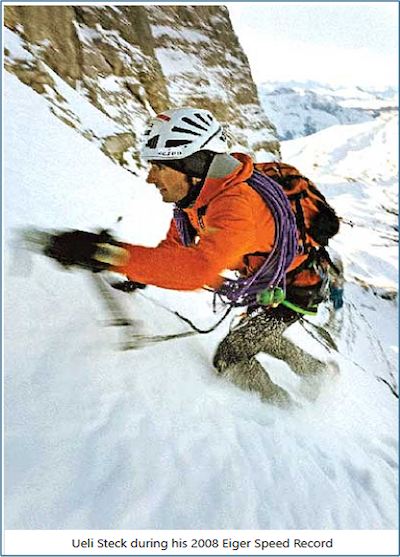

In 2015 the Swiss climber Ueli Steck climbed Heckmair’s route top to bottom in 2 hours 2 minutes. Now you can get a train to take you up the side and over the top.

You can climb the Eiger by laying siege to it, with a team, with all the safety accessories, wall-hanging bivouacs and mountain stoves, cold weather overnight gear etc etc. Or like Ueli you can go Alpine style, one rope, very lightweight, very fast, very simple: one simple objective achieved.

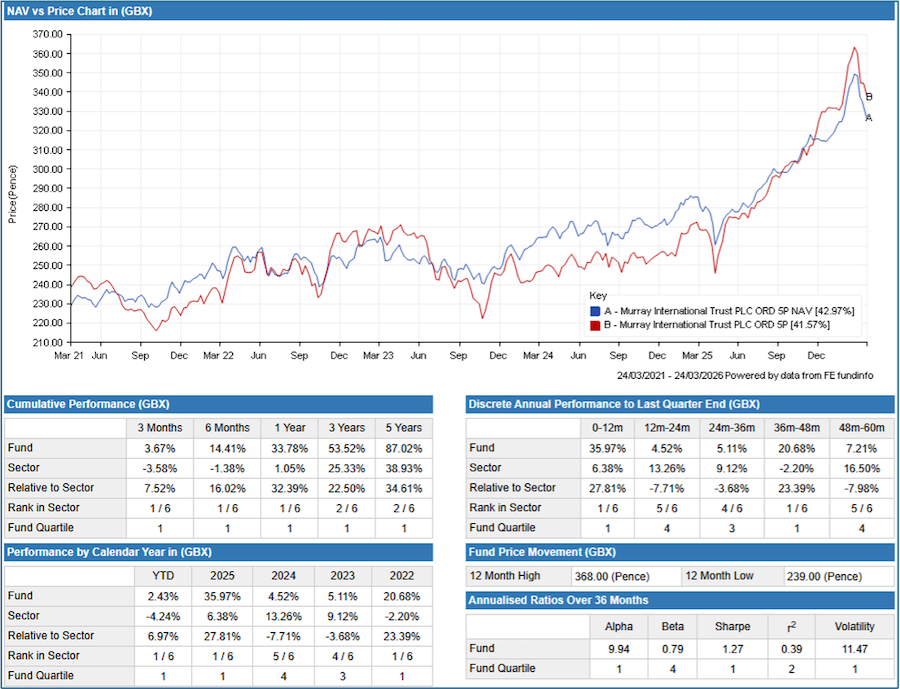

/2. Murray International

Murray International is an investment trust that runs multi-currency hedge reviews, analysis and due diligence on Mexican airport operators, as well as Taiwan Semiconductor. They measure and monitor dividend cashflows from their investee companies, the current conversion rates and the projected rates for when the money is paid. They do this across the whole £2 billion portfolio, with each investment at around £40 million. For your pension, you can do a Ueli and buy the shares in Murray International, take the income quarterly, clean, reconciled, all in GBP. Or you can do the Heckmair method – get all the information and tools you might need, get a team together for expertise, try and work out the investing routes yourself and execute the 50 share trades to get the same diversification. Note, at best, you’ll just get to where Murray International is, at worst, you’ll implode and bottle out when you can’t reconcile and project what you’re doing to your lifetime savings.

Having Murray International at your keyboard fingertips and choosing to lose yourself in ‘Yes but … asset allocations’ conundrums is genuinely like having a dog and barking yourself. Hire the team at Murray as your own private office investment team. (Disclaimer: the directors are proud to say we are shareholders in Murray International and have been for years – we love it).

/3. Law Debenture

Law Debenture is a 137-year-old trust; it started in 1889, which happened to be the same year that Coca-Cola and the Wall Street Journal started. [Pub quiz note: it also happens to be the year the first jukebox was invented, in San Francisco, though no record exists of what was playing on it].

The trust is unique – it owns its own trading subsidiary, Independent Professional Services Ltd (IPS), which provides trustee and corporate governance services. It is 16% of the net asset value of the trust and has a simple objective of real capital growth and ‘steadily increasing income’. The investment management is run by the very experienced team of James Henderson and Laura Foll – a more calm, focused and competent duo would be hard to find.

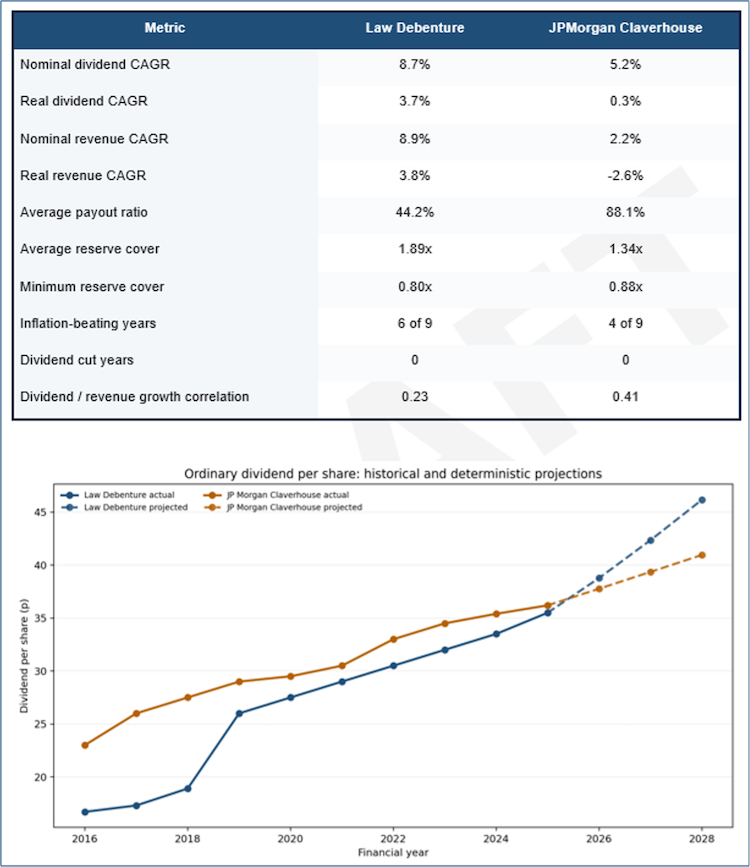

For you and I it’s the data that counts; last week James visited us in Chancery Lane along with Denis Jackson, the CEO, armed with summaries of the recent performance, examples of investments they hold, details of IPS’ c10% annual revenue growth since 2017 et al. However, we didn’t go through the stats – we didn’t need to. Our job is to research and recommend and we’d already been through all the data relevant to us. This is a snippet from our paper comparing projections of future dividends from Law Debenture with JP Morgan’s Claverhouse. Clients need us to have a handle on next year’s income, not last year’s.

/4. When data lies and hallucinates – the acute danger of DIY.

The data tools we use, some of them hosted by the Artificial Intelligence giants, allow us to contrast and analyse large swathes of Excel data within multiple sheets in a workbook. However, it can only calculate and interpret the data it sees. It can extrapolate, but only based on the trends and similar inputs – and trends are based on historical data.

“A.I. tools can’t sit down with James & Laura.”

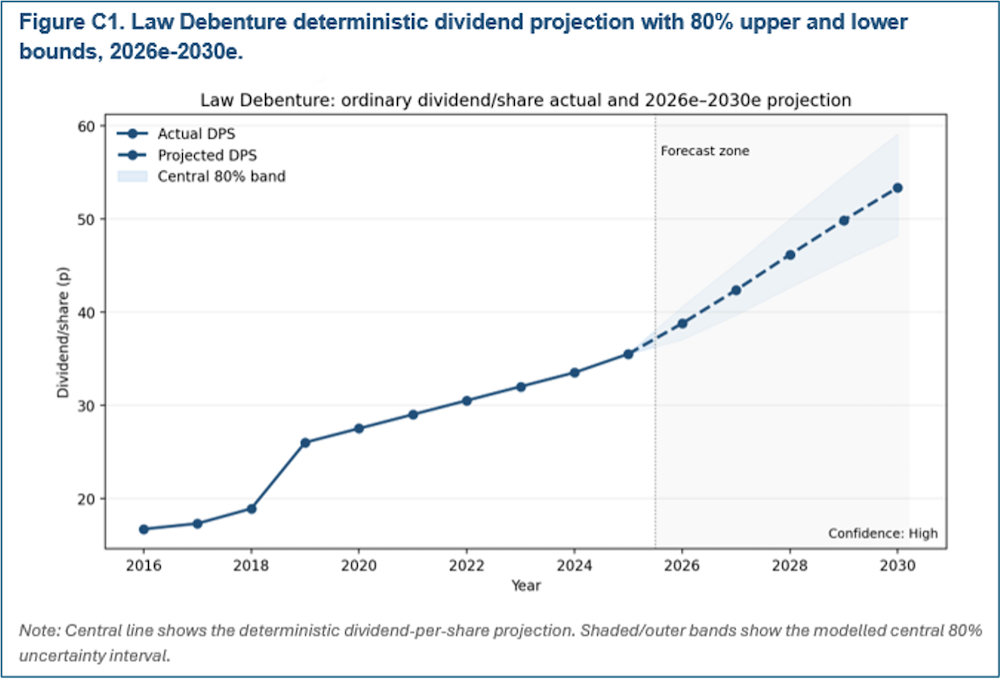

The interpretation produces this optimistic chart, showing the expectation of the future dividend growth at 9% pa based on historical trends.

DIY investors beware: the manager’s view of future dividend growth is much closer to the 3.8% annual increase that we use in our current modelling. No data interpretation, however complex, can take into account the views and information forming the decisions being made by James and Laura, and that is the purpose of having human managers. Does it work? I should say so:

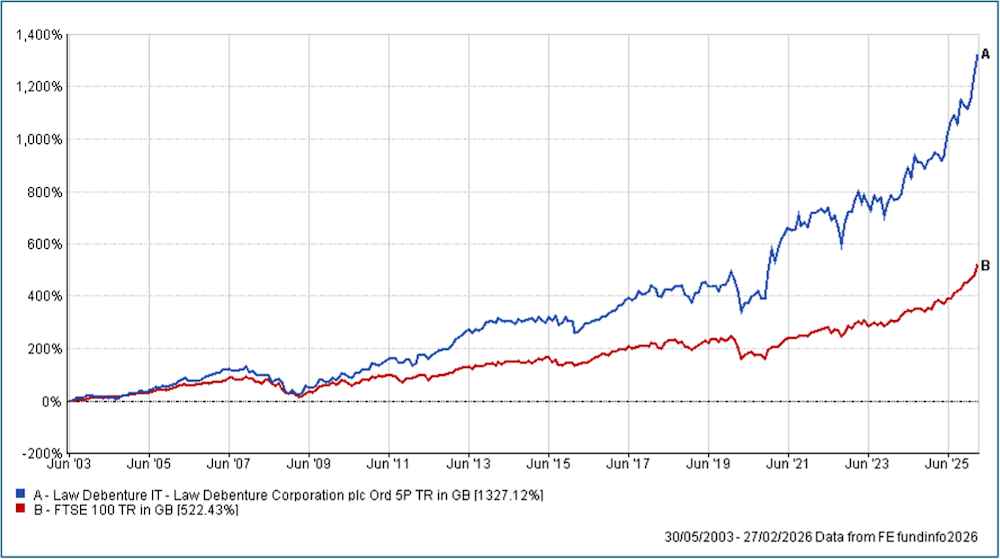

This is the total return since James became lead manager of the trust, so when you read the marketing headlines from the passive fund sellers saying active doesn’t beat passive, you know that’s simply not true. Since James took over he’s beaten the FTSE 60% of the time. More, the average annual dividend increase in the dividend in his tenure has been 8% pa with the mid median value 5.4%.

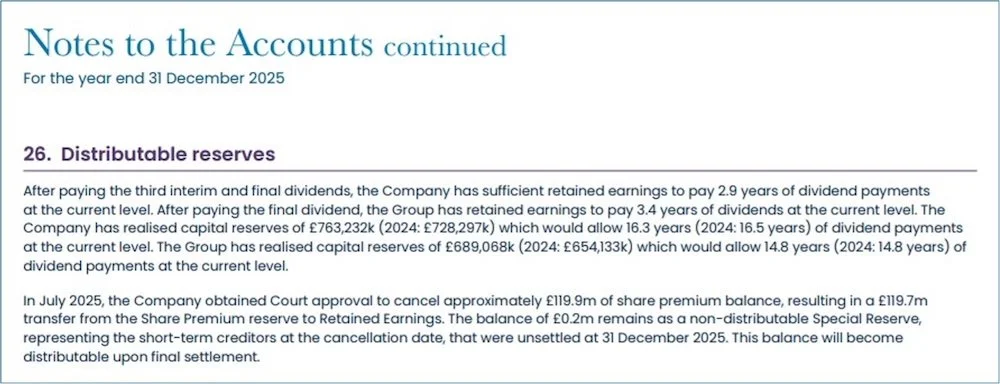

Importantly – very unusually – we found Note 26 in the report and accounts for 2025:

This is brilliant for us as the Board here has done what we do manually for all our investment assets; this is how to build a portfolio of sustainable income for your retirement.

“Disclaimer: the directors do most certainly hold shares of Law Debenture in their own SIPPs.”

/5. What the client wrote…

Hi Doug & Jim,

Back in 2013/2014 we asked you what you considered to be a good way of getting money out of our estates to our grandchildren to whom we had recently given £x per child, and we did not want them to be able to access any future funds for the foreseeable future.

Your suggestion was to fund a pension for each grandchild, and we have done this to the maximum allowed of £2,880.00pa per child and we have now been doing this for 11 years. It has therefore “cost” my wife and I a total of £31,702 per grandchild and we will continue to fund these pensions as long as we are able from excess income and therefore escaping IHT and grows in the name of the grandchild.

We asked our granddaughter Alice what her pension pot was worth and she has informed us that hers is worth £74,084 as at 27th February 2026, and our contribution for March 2026 of £240 is yet to be added. Now we all know that the stock market, where it is invested through Fidelity, goes up and down and because of the Middle East problems it will take a substantial hit.

This was a great suggestion of yours and if you ever want to, please use the above as an example to give weight to any suggestions you make to other clients in this area. Our grandchildren should be very grateful to you both!

Kind regards, NT

About the author

Doug is the Founder and CEO of Chancery Lane. He has worked with personal investing since 1989, specialising in income investing for the last fifteen years, firstly with Old Mutual and running his own award winning business since 1995. Doug is chartered with two professional institutes, CISI and CII and holds the Certified Financial Planner licence.