Never judge your retirement by cost.

by Doug Brodie

[1] Commitment.

Without tumbling into the rabbit hole of Western politics, it is likely to be true that if the nine Prime Ministers since Thatcher were asked what their priority had been in their tenure, you’d get nine different answers. If they all are allowed to set their own benchmark, then how can we tell who’s succeeding and who’s not? What are they measured against?

Gordon Brown doesn’t usually hit Top of the Pops but from 2007 – 2010 he had protection of the UK from the implosion of the world’s banking system as his main task. Like Major, May and Sunak. Sir Keir was put in place to reduce political excitement and maintain predictable stability – it’s clearly very hard for elected MPs to sit on their hands and just keep on doing what people want them to do.

The politicians lay out a manifesto which says what they will do if elected; as we know, most find it hard to stay with those electoral promises, so you/we don’t get what we expected. As much as political events constantly change, so do economic and investment scenarios. As I write this at 11 in the morning, there are around 120 new emails in my inboxes, the majority telling me about AI in China, income from various funds, a new Japan fund, how the US-Iran deal affects Asian equities, why ‘alts’ and private equity are attractive for retail investors, etc., etc., etc. – all begging for my attention.

I love what we do because it’s very simple – the simple part is getting the expectations between you and me aligned; we both expect to see the same outcome. The reference point we both use is the monthly or annual income that is needed to meet your living costs and aspirations. Income is binary, it’s either there or it’s not. Our job is to be aware of the news flow and know what to ignore, and we do indeed ignore 90% of the noise. Moody’s may be right about ‘European banks’ exposure to US business development companies’, but we only follow income, that keeps our role simple.

It ain’t easy.

Keeping applied to a commitment, whether that be to the voting public or to you, the client, is not easy. We can look at our desks, emails, texts and there are lots of distractions, sometimes it’s really difficult to keep focused. As we get older, that doesn’t improve, and then there’s the dopamine addiction: change is one of the primary triggers for dopamine release. Incentive salience is the term that describes how there are embedded stimuli that drive us to approach a reward, like food, or drink or affection or natural enjoyment.

We are free to write our own cheques, spend what we want, but we know we need to commit to our flexible financial plans, within the guardrails of prudence. We might be older but that doesn’t mean we’re always grown up, and usually, an amount of alcohol to remove the defensive wall from our inhibitions reveals that we haven’t forgotten what it’s like to have a water fight, to pinch the last biscuit, to drive through a puddle. The childhood element is not deleted, it’s just stored away.

Historian and philosopher Will Durant on staying young:

"Childhood may be defined as the age of play; therefore some children are never young, and some adults are never old."

That’s why some eyes always have a little sense of a twinkle in them if you look long enough.

“If you’ve come to Chancery Lane looking for planning or investment advice on anything other than income, you’ve come to the wrong place.”

[2] Every day’s a school day – the tokamak, and why it’s important.

As you saw in last week’s email, ‘skin in the game’ is a good yardstick when reading commentary intended to inform you. There are firms better than us at macro asset allocation, at tech investing (including crypto), emerging markets or commodities, however, for the unexciting predictability of reliable, inflation-defeating lifetime income, we’d raise our hand.

The trigger for this mini-rant is an email from a very, very large platform this morning, with an extensive number of DIY investors, promoting just five funds from the 4,000+ UK universe (“Here’s 5 great funds for income”). The recommendation is written by ‘… an investment writer, previously a journalist’. Of the funds recommended, over the past 5 years, the annual returns include one at 3.4% and one at 3.5% - when the better cash deposits were 4% per year.

I’ve also just read advice in Investors Chronicle to a reader seeking help with a £50,000 ISA, including the line “I think your investments in emerging markets are a clever move as sentiment is shifting towards the region”. Que??? I think that line is fine in a morning briefing at JP Morgan or the Rolls-Royce pension fund, but for a small retail investor, that’s just missing the point. Don’t fiddle, it’s not Lego, it’s not a loose thread on your jacket, it’s your financial security, it’s the future income that you will rely on to pay your living costs.

“Your pension: Don’t fiddle, it’s not Lego.”

When you work for an employer, you do it (usually) five days a week, for 46-odd weeks a year, stretching over 30 / 40 years. You are unlikely to chop and change frequently or start unpicking the role of the employer or its owners, etc. Equally, if you have a final salary pension, you’re unlikely to have ever questioned the investment manager or the scheme actuaries (unless you’re a trustee). Just because you can see the innards of your SIPP, ISA or other money purchase pension doesn’t mean your opinion is needed.

In the same vein, we have several clients who are current or former fund managers (some running £billion funds) – they are engaged, they understand the market terminology and volatilities, however, they also do not pick at threads. They understand the difference between capital and income, and between real assets (shares) and derivatives, long and short, $ and £. They are not income investors nor pension specialists; they choose to outsource that work to us. They don’t fiddle, and we like them for that.

What retail pension investors benefit from is understanding how income is generated (look for free cashflow), how it becomes reliable (strength and reserves) and how it deals with inflation (holding stocks or assets that go up with inflation).

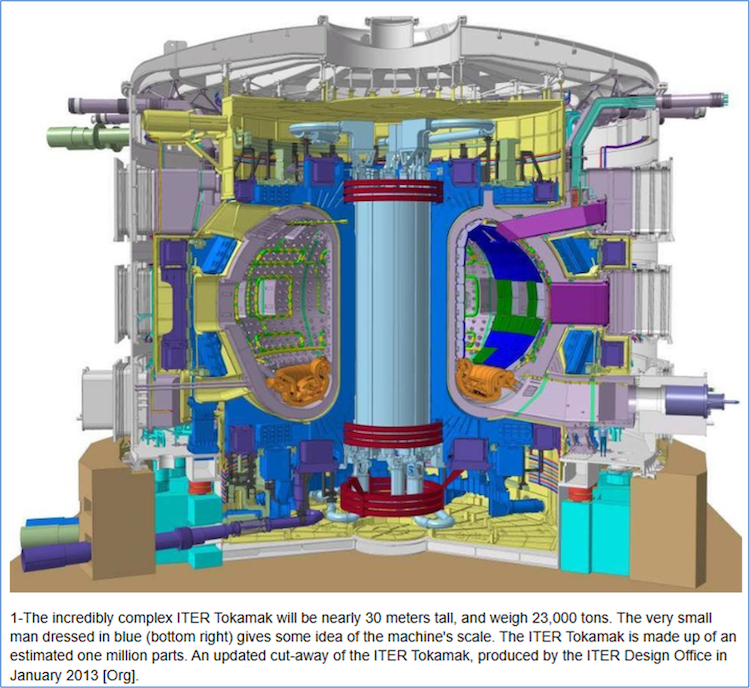

This is a diagram of the ITER tokamak.

ITER is the world’s largest ‘magnetic confinement plasma physics experiment’: it’s all about plasma energy, an experiment to see if ‘burning plasma’ experiments can become self-sustaining, meaning generating more heat than the energy required to start them – a bridge to carbon-free power plants. We don’t need to know how our electricity is generated, just how to be careful – more what NOT to do than what to do – and to be reassured that it is reliable.

In case you’re interested, to achieve fusion, the plasma in the tokamak must reach 150,000,000 centigrade. Note, the sun’s core is 15 million centigrade – I know because NASA tells us, I have no idea how you take that temperature!

With that level of academic and scientific knowledge around, pension income is really not that hard to manufacture.

[3] "We can't change the year we're retiring: we need income irrespective of market values."

None of us gets to choose the year we retire. It arrives with a birthday, or simply the moment we decide that enough is enough. Markets, sadly, don't check our calendar. If you retire into a falling market while selling units to fund your spending, you lock in those losses for good. The very same pot, retired into a rising market, can last decades longer. This is sequencing risk, and it quietly catches many newly retired people unaware.

But here is the reassuring part, you can sidestep most of it. When your income comes from the dividends and interest your investments pay out, the day-to-day price of your holdings matters much less. Well-run companies and funds keep paying, and growing, their dividends through the bad years as well as the good. Our research at chancerylane.net shows just how dependable that natural income can be.

Right now, markets sit at high levels, and that carries a consequence many people miss. Price and income pull in opposite directions, so when prices are high, yields are low. A pound invested today buys you less income than the same pound would buy after a fall.

Take a simple example. Say an income fund pays 5p a year for every share, and the shares cost £1 each. The yield is 5p divided by 100p, which is 5 percent, so £10,000 buys 10,000 shares and £500 of income a year.

Now suppose the price later eases to 80p. That same 5p dividend becomes 5p divided by 80p, a yield of 6.25 percent, and your £10,000 buys 12,500 shares paying £625 of income. That's £125 more every year, for the same outlay, simply because you bought at a better yield.

This is why here at Chancery Lane we phase, drip-feeding the money in rather than committing it all at one potentially expensive moment. And occasionally, when yields look especially thin, we defer, holding back until the income on offer improves. Phasing pulls in two directions at once. On defence, it spreads your buying across time, so no single day's prices get to decide your whole retirement. Start when markets are high and you've only committed a slice. Should they fall, your later tranches buy more income for the same money, and that dreaded bad first year loses much of its bite.

It's productive as well. Every slice you invest goes straight to work, paying dividends and interest from the off. Those payments can be reinvested while you ease in, or drawn when you need them, so your capital earns its keep from day one, while idle cash just loses ground to inflation.

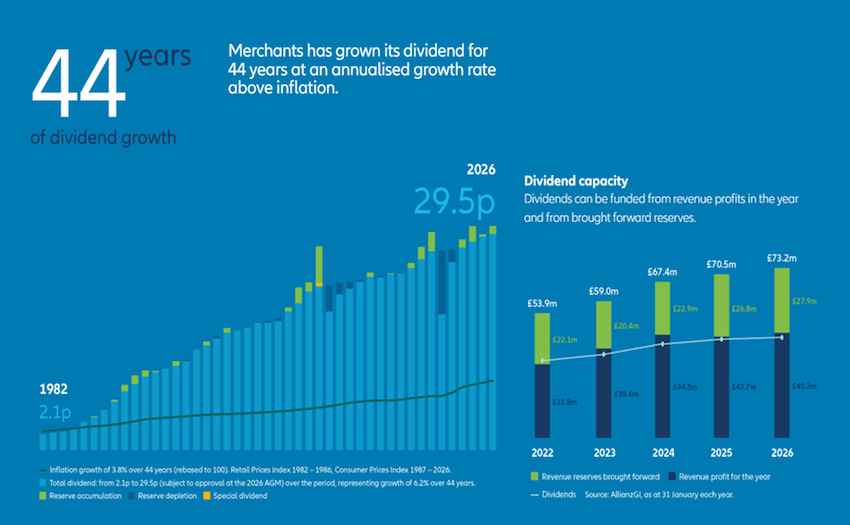

This chart illustrates quite clearly how Merchants Trust has used its reserves to pay an increasing dividend to its shareholders even through the dotcom 3-year market collapse, 2008’s credit crunch collapse and 2020’s Covid collapse. Income and capital are NOT correlated, they do different things.

The heart of the matter is that income built on dividends and interest keeps arriving, whatever the market is doing on the morning you need it. The retirement date you couldn't choose then loses its sting, because your income doesn't depend on it.

And here’s one last look at that Greek taverna lunch:

About the author

Doug Brodie is Founder and CEO of Chancery Lane Income Planners. He has specialised in retirement income for over thirty years and is Chartered with both the CISI and CII. This article is general information and not personal advice. Tax rules can change, and the impact of any planning depends on your specific circumstances. Capital is at risk and past performance is not a guide to future returns.