Other people

by Doug Brodie

[1] Don’t assume the wealth of others

We spend our working lives building towards retirement. Decades of saving, planning, and telling ourselves it will all be worth it. And for most people, it is. But the numbers tell a more complicated story and we think they are worth sharing. We know that there’s little point in comparing ourselves to others, and as it happens, we know there is a lot more disparity in the financial position of folk, no matter what it looks like from the outside.

A new car is rarely bought for cash, and £10,000 for health insurance may be a highly valued ‘asset’ for some, whilst NHS queues are acceptable for others. That second home may be rented or have a material mortgage on it, or the wealth you see may all be inherited, or be due to parental or sibling direct help – imagine the property developer who is able to feed contracts to his son’s building firm. Nepotism is not often a bad thing, and you rarely see it. Others have excessively generous employment pensions – we’ve seen final salary pensions measured in six figures, unjustifiable in today’s world.

Here is the first statistic. Only 51% of UK baby boomers are currently on track to meet their retirement income goals. That means roughly half are heading towards a shortfall, often without knowing it. Yet among those who take professional financial advice, that figure climbs to 83%. The difference is not luck, and it is not complicated. It is simply having someone help you see the full picture before it is too late to act.

The second number surprises most people. The average UK retiree spends around £22,000 a year (note: that’s a very broad national average). That sounds reasonable - until you compare it to the Pensions and Lifetime Savings Association's benchmark for a comfortable retirement, which sits at roughly £44,000 for a single person. Nearly double. The gap between what people spend and what they actually need for a genuinely comfortable life is one of the most important conversations we can have. And far too few people are having it.

The third fact is more encouraging. Research by SunLife found that 65% of retirees say they are happier after retiring than when they were working. The happiest among them have something in common - they spend on experiences rather than possessions. Holidays, hobbies, time with the people they love. It turns out the best use of your money in retirement is not things you can own. It is moments you can remember. Your happy time may be organising a grandchild, fiddling with a carburettor, learning a new language, bagging Munros, paddle boarding in the Caribbean, growing vines in Crete, refurbing that house in France, carving oak, mastering tennis, gold, padel, flying – skills and hobbies.

I keep a notebook. Nothing clever, just a running file where I drop the things that catch my eye during the week. A line from a client call, a chart, a quote that lands and will not leave. Most of it goes nowhere. Some of it nags at me until I sit down and write it up properly.

What follows is a handful of these, each one its own short subject. Read the ones that interest you and skip the ones that do not. But there is a thread running through them, as there usually is. It is about expectations, patience, and the quiet business of having enough.

[2] Retiring too early, and the boredom nobody warns you about

Here is something the brochures rarely mention. One of the most common complaints in retirement is not money, it is boredom. When the alarm stops, the diary empties, and the sense of being needed quietly fades, a good number of people find the early months harder than they expected.

The research backs this up. Studies of older adults consistently find that a sense of purpose falls after full retirement, and that a lower sense of purpose travels alongside more anxiety and lower mood. One often-quoted figure suggests roughly a quarter of retirees show symptoms of depression, a higher rate than among those still working. I would treat the exact percentage as approximate, but the direction of travel is not in doubt.

This matters for financial planning, because money is only half of it. The other half is having a life worth retiring into. Before you fix the date, it is worth asking what Monday morning is actually for. Voluntary work, grandchildren, a long-postponed project, a part-time return on your own terms. The pension funds the freedom, but you still have to fill it.

[3] The man who sold at the bottom

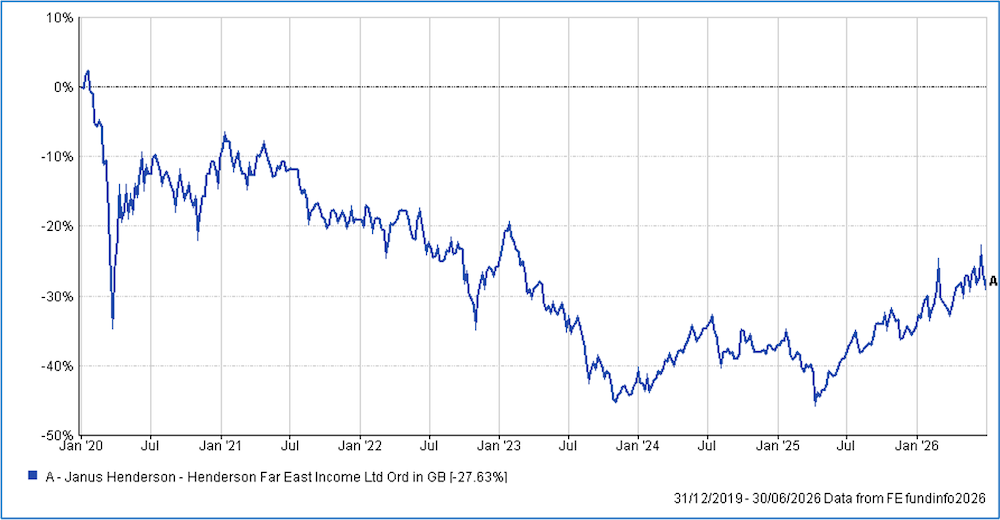

In 2020 a man rang me, badly worried. He had just retired, put a large slice of his self-invested pension into a single income trust, Henderson Far East Income and watched it fall 25%. He had bought it for the yield. Now he was convinced he would run out of money.

I owned the same fund, still do. I told him it would probably be fine, because I had bought it for the same reason he had, the income it paid, and the income had not stopped. He never came back to me. I have long suspected he sold near the bottom, which would have turned a paper wobble into a permanent loss of real capital, at the very worst moment, the start of his retirement.

My own holding took years to claw back to a small profit on the share price. So what. Across that whole stretch, it kept paying me a high and rising income, which is the only reason I held it. The fund still yields somewhere around 9% today and, according to its manager, has raised its dividend for roughly 16 consecutive years (a figure worth checking against the latest factsheet). The share price is the noise. The income is the point. Its last annual dividend is 25.05p, the price back at the end of 2020 was £3.26, so the yield to cost is 7.7%.

“More, for the purchase price of £3.26, I have now had a total £1.28 paid to me in dividends, almost 40% of the cost. Deduct that from the outlay means I am still £1.96 out of pocket yet for that net cost I have 25p per year of dividends – a 12.6% yield on that remaining cost.” Don’t worry, be happy, as the man said.

[4] On having enough

Marcus Aurelius is supposed to have written that very little is needed to make a happy life, and that it lies within yourself, in your way of thinking. The attribution to his Meditations is widely repeated, though I cannot point you to chapter and verse, so please take the wording as the spirit of the man rather than a verified quotation.

The finance writer Morgan Housel makes the same point in plain money terms. Imagine two people. One earns 8% a year and needs half as much to feel content. The other earns 12% but spends as fast as the money compounds. The first is better off, despite the lower return.

His wider argument is the one I keep coming back to. Reducing what you need has the same effect on your finances as increasing what you earn, and it is more within your control. An investor might grind for years to add a fraction of a percent to returns, while two or three per cent of comfortable, unnoticed spending sits quietly in the background, available to anyone willing to look for it. This holds true whether you spend £15,000 a year or £15 million. Mr Micawber was right.

[5] Twenty holes in the punch card

Warren Buffett once told a room of students that he could improve their lifetime results by handing them a card with just 20 punches on it. Every investment they ever made would use one punch. Once the card was full, they were finished, with no more decisions allowed.

His point was not really about the number. It was about behaviour. If you knew you had only 20 chances, you would weigh each one properly, wait for the ones you understood, and ignore the rest. The card forces patience on people who would otherwise fidget.

He gave that talk at the University of Georgia around 2001, and it has aged well. Most of the harm in a private portfolio comes not from bad investments but from too many of them, bought in a hurry and sold in a fright. For someone drawing an income in retirement, the discipline is the same. Own a sensible spread of good, income-producing assets, then sit on your hands. The temptation to tinker is strong. The punch card is a useful answer to it.

[6] Do not buy the dip, and do not dump either

Jason Zweig, who writes the Intelligent Investor column for the Wall Street Journal, has a line I find steadying when markets lurch. When prices tumble, he argues, the useful question is rarely whether to buy the dip or bail out. It is to revisit why you own what you own in the first place.

That sounds almost too simple, and that is rather the point. If you bought an income-producing investment because it pays you a reliable, growing income, a fall in its price changes the headline, not the reason. The cheques keep arriving. If anything, a lower price buys more income per pound for anyone still adding to the pot.

The trouble is that falling markets do not feel like that in the moment. They feel like a verdict. The discipline is to go back to your own original reasons, written down ideally, and check whether they still hold. Usually, they do. The market mood swings far more than the underlying businesses paying your dividends and confusing the two is how good plans get abandoned at the worst possible time.

[7] Probability is not the same as statistics

Allow me one slightly nerdy detour, because it explains a great deal of bad forecasting. Probability and statistics are taught side by side, yet they do opposite jobs. Probability starts with known odds and asks about unseen outcomes. Toss a fair coin five times, what are the chances of four or more heads? You know the odds in advance, and the result has not happened yet.

Statistics runs the other way. You have the observed data, a pile of messy real numbers, and you are working backwards to the parameter you cannot see, such as the true average return of a market. You estimate it, and you put a range around the estimate, knowing it is exactly that, an estimate.

Why should an investor care? Because a great deal of confident commentary treats statistics as though it were probability. A forecaster points at the past 20 years and announces what comes next with the certainty of someone reading coin odds. They are doing no such thing. They are estimating from limited data, and the honest version always arrives with a range and a shrug. Be wary of anyone whose forecast turns up without either.

[8] A Beggars Banquet of consequences

There is a famous line, usually given as Robert Louis Stevenson saying that sooner or later we all sit down to a banquet of consequences. It is a fine sentiment. It is also, strictly, a misquotation. What Stevenson actually wrote, in an 1884 essay called Old Mortality, was about the game of consequences we all sit down to. The banquet version appears to have been a later rewrite, repeated so often that it stuck. I rather like knowing the difference, and I suspect Stevenson would too.

The thought underneath it is sound, and it pairs with two others from my notebook this week.

The first: praise others freely, since it brings them peace of mind, and expect no praise yourself, since that brings you peace of mind.

The second: what looks like steady commitment can sometimes be fear wearing a respectable coat. Are you holding to a course because it still serves you, or because it is simply the one you know?

None of this is a reason to tear up a good plan. It is a reason, once a year or so, to sit down honestly with your own consequences, financial and otherwise, and ask whether the path still fits. That, in the end, is most of what a decent review is for.

Have a good week, or if you’re on holiday near the sea or a lake, have a Hobie day!

Doug

About the author

Doug Brodie is Founder and CEO of Chancery Lane Income Planners. He has specialised in retirement income for over thirty years and is Chartered with both the CISI and CII. This article is general information and not personal advice. Tax rules can change, and the impact of any planning depends on your specific circumstances. Capital is at risk and past performance is not a guide to future returns.