“What’s it worth?” Valuing the UK state pension for an individual.

by Doug Brodie

REPLICATING THE UK STATE PENSION

A Plain-English Example to Inflation-Protected Retirement Income Using UK Gilts

/1. Executive Summary & Purpose

The UK State Pension is one of the most valuable financial assets an individual can possess. Its value does not come merely from the weekly cash payout, but from its core feature: it is contractually guaranteed by the government and completely protected against inflation. For an individual receiving the full State Pension of £12,547 per annum, replicating this secure stream of income independently is a common challenge — especially for a surviving spouse facing the abrupt loss of half of a household's joint state pension income.

This report evaluates how a retail investor can use UK Government Bonds (known as 'Gilts'), specifically the 0.25% Index-Linked Treasury Gilt maturing in 2052, to build an independent income stream that perfectly matches this £12,547 baseline and grows predictably to offset the cost of living.

/2. Core Concepts Explained Simply

Before reviewing the numbers, it is essential to understand the basic building blocks used in this strategy, stripped of complex financial jargon:

What is a Gilt? A Gilt is an official 'IOU' issued by the UK Government. When you buy a gilt, you are lending money to the government. In return, they guarantee to pay you a small interest payment twice a year (called a coupon) and promise to pay back your original full loan amount on a set date in the future (the maturity date). Because the UK government has never defaulted on its debt, gilts are considered among the safest investments on earth.

What is an Index-Linked Gilt? A standard bond pays a fixed amount of cash. If inflation spikes, that fixed cash buys fewer groceries. An index-linked gilt fixes this by automatically scaling up both its regular interest payments and its final cash payout at maturity in line with the UK Retail Prices Index (RPI) inflation tracker. If prices double in the economy, your payouts double, fully preserving your purchasing power.

Clean Price and the 'Pull-to-Par': Bonds trade daily on an open market, and their prices rise and fall. 'Clean Price' represents the core cost of the bond before factoring in temporary accrued interest. If a bond has a face value of £100 but is priced at £61.66, it is trading at a significant discount. Over time, as the bond gets closer to its final maturity date, its market price naturally gravitates upward toward its full payout value. This inevitable journey is known as the 'pull-to-par' effect.

/3. Three Strategies to Replicate the Income

To secure a guaranteed income of £12,547 per year that grows smoothly at an assumed inflation rate of 2.5% per annum for the next 26 years, an investor can choose between three distinct routes:

Strategy A: The Coupon-Only Approach (Capital Intact)

In this strategy, you purchase enough bonds so that the tiny regular interest payments alone generate your target income. Your core investment capital is never touched or sold down, meaning that when the bond matures in 2052, your entire multi-million-pound investment is paid back to you, fully uprated for inflation.

Because the real interest rate on the 2052 bond is very low (0.25%), you must buy a massive volume of bonds to hit your income goal. At a market price of £61.66, this requires an upfront capital outlay of approximately:

Cost: £3,060,244.

This represents the cost of absolute certainty in its purest form, leaving an enormous, inflation-protected inheritance behind for beneficiaries.

Strategy B: The Single-Gilt Drawdown Approach (Capital to Zero)

Instead of living only on interest, this strategy systematically chips away at the core capital itself. Each year, you collect the interest payment, and then you sell off a small slice of the bond on the open market to top up your cash to the target income level. Over 26 years, the account balance steadily winds down until it hits exactly zero at maturity in 2052.

Because you are consuming the capital rather than preserving it, the upfront cost drops drastically from over £3 million down to approximately:

Cost: £240,420.

While financially accessible, this strategy carries a severe hidden trap: the 'Savings Account Illusion'. A gilt is not a liquid cash account. If you are forced to sell precise slices of a single long-dated bond on the open market every single year, you are completely exposed to whatever price the market dictates that day. If market interest rates spike, bond prices crash, forcing you to sell far more of your bond than planned, threatening to empty your account prematurely.

Note: it is only the coupon and the maturity sums that are index-linked and guaranteed by the government. Selling part of the gilt each year is at the price in the market – you are selling to other secondary investors, not to the government.

Strategy C: The Index-Linked Gilt Ladder (The Recommended Alternative)

A gilt ladder completely eliminates the market risk of Strategy B while keeping the low cost. Instead of putting all your money into a single bond maturing in 2052 and selling chunks off blindly, you distribute your budget across a series of different index-linked gilts timed to mature in a staggered sequence - one bond maturing in Year 1, another in Year 2, another in Year 3, and so forth.

When a bond matures, the UK government pays you the full, inflation-adjusted cash value directly. By aligning these natural maturity dates with your annual retirement spending timeline, you get cash in hand perfectly adjusted for inflation, and you never have to sell a single bond early on the open market. This eliminates interest rate volatility entirely, providing an almost accurate replication of the State Pension. Due to the state scheme having a floor of 2.5% - the Triple Lock – the index-linked gilt will not match this when inflation falls below 2.5%.

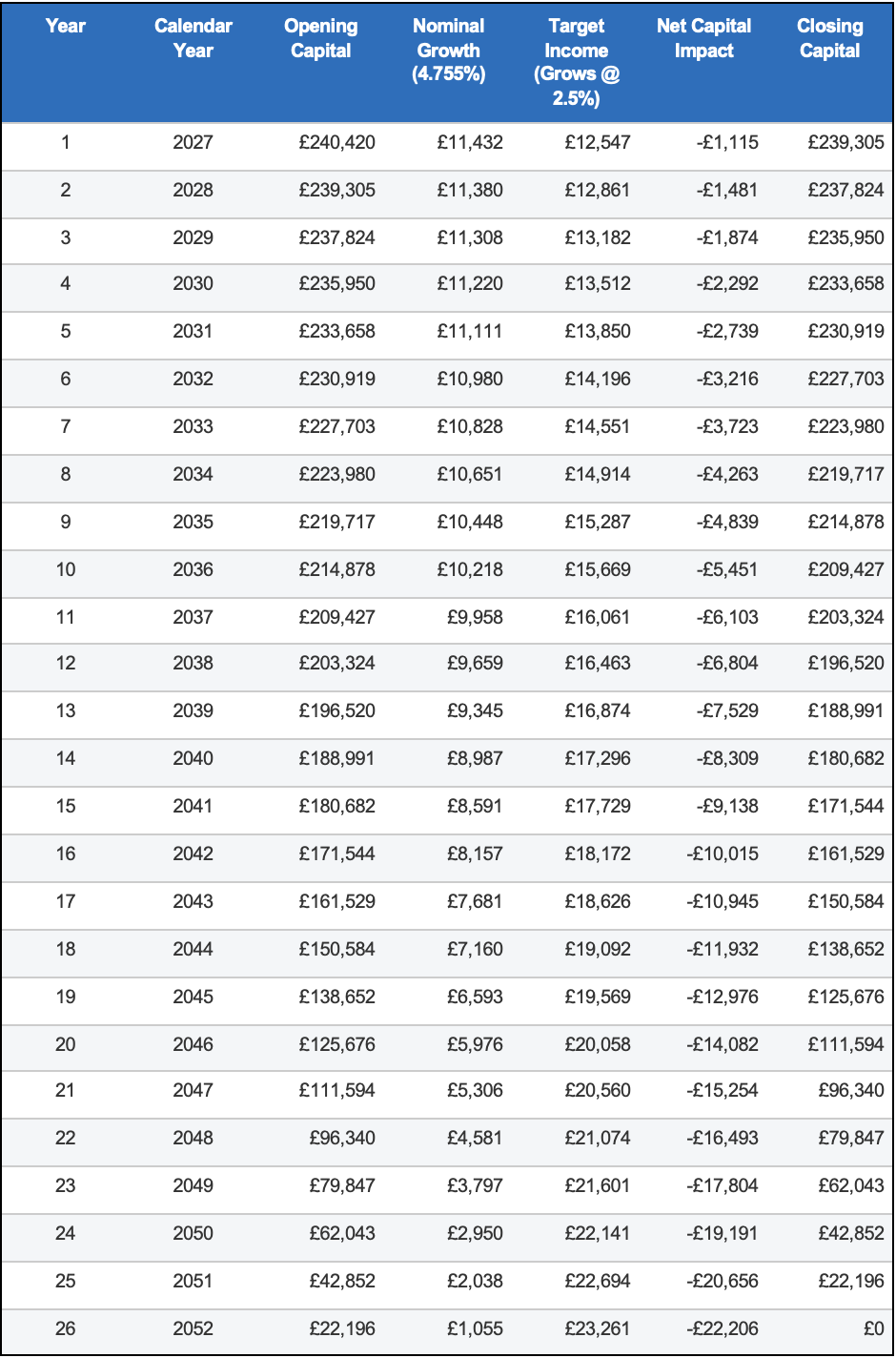

/4. The Corrected Year-by-Year Financial Ledger

To clear up the mathematical and accounting gaps found in typical advisory projections, the table below maps out a mathematically precise, self-balancing ledger for the Drawdown Strategy (Strategy B) in nominal terms. It assumes a starting capital of £240,420, a fixed 2.5% inflation rate, and an implied total nominal return of 4.755% per annum.

Closing Capital = [Opening Capital + Nominal Growth] minus Target Income

*Note: Total nominal payments distributed to the investor over the 26-year timeline equal £451,839, funded by a combination of bond interest, capital sales, and structural market price appreciation.

/5. Critical Risks & Practical Realities

While replicating a pension with gilts provides great structural security, a retail investor must remain mindful of four critical real-world distinctions:

1. The 2030 Inflation Metric Structural Shift: In 2030, the UK Government will officially change how index-linked gilts calculate inflation, shifting from the traditional Retail Prices Index (RPI) to a metric aligned with CPIH. Historically, CPIH runs roughly 0.5% to 1.0% lower than RPI. Because the real State Pension is guarded by the 'Triple Lock' mechanism (guaranteeing it outpaces standard inflation when wages grow faster), a gilt-based model will likely experience a slight tracking gap post-2030 and underpace a true state pension.

2. Taxation Differences: Outside of tax-sheltered wrappers like an ISA or a SIPP, gilt interest coupons are subject to regular UK Income Tax. However, a major tax benefit for retail investors is that any capital gains generated by the bond's 'pull-to-par' discount appreciation are entirely exempt from Capital Gains Tax (CGT) under current UK legislation.

3. Payout Frequency and Cash Smoothing: The UK State Pension is distributed as a smooth, predictable payment every four weeks, making it ideal for matching monthly household utility and living bills. Gilts, by contrast, distribute their interest lump sums only twice a year. This requires the investor to maintain a small, disciplined cash buffer in a standard checking account to smooth out seasonal cash flows.

4. Inflation Drag: The inflation rate applied to the linker is the rate declared three months previously, whereas the state pension uses one RPI figure, that in September.

/6. Conclusion & Professional Guidance

For a retail investor looking to replace an inflation-linked pension stream safely, investing roughly £240,000 into a structured index-linked gilt framework provides a highly secure solution. However, to guarantee success and eliminate market pricing dangers, investors should avoid concentration in a single bond and instead deploy a properly diversified index-linked gilt ladder.

If you want to use an annuity, it’s around £230,000.

If you want to use income and capital drawdown for a finite period of 26 years, it’s around £240,000.

If you want to use income only from an index-linked gilt with a real yield of 1.65%, it’s around £760,000.

If you want to use income only from the 2052 0.25% gilt at £61.66, it’s around £3 million.

Disclaimer: This report is purely for illustrative and educational purposes and does not constitute formal financial, tax, or legal advice. Gilt market prices change daily, and real-world results will depend entirely on actual inflation figures and legislative changes.