Wish you were here.

The album was released 50 years ago, I was prepping for ‘O’ levels … you?

by Doug Brodie

/1. The mismatch

Pink Floyd released the song in September 1975, on an album of the same name. The lyric is, in essence, about absence - originally written for Syd Barrett, the band's first songwriter, who by the mid-1970s had withdrawn from music into a private illness from which he never quite returned. Fifty-one years on, the song is still reached for at funerals and memorials. It works because the words are simple and the feeling is universal.

Every long marriage eventually faces the same arithmetic. One day, one of the two of you sits down on the sofa where two of you used to sit. The kettle still boils, the post still arrives, the bins still go out on a Tuesday. But one chair, one cup, one signature, and - the part this article is actually about - one income, are no longer there.

This is the corner of retirement planning that nobody quite wants to write about. So, we will write it now, in advance, before the moment arrives, while there are still two of you to read it together and, very probably, disagree about it.

The arithmetic of the surviving spouse is unusual and worth understanding before it arrives. Household running costs do not halve when the household halves. Council tax falls by 25% on the single-person discount, not by 50%. Heating is the same. The car is the same. The mortgage, if there is one, is the same. The holiday for one usually costs rather more than half the holiday for two. What changes - sharply and immediately - is income. One of the two State Pensions stops in the week of the funeral. Many private pensions follow, in part or in full. The widow or widower is left with most of the bills and considerably less than half of the income.

That mismatch is the thing this article is about. Everything that follows flows from it.

/2. What dies with you, what does not

On the first death, the surviving spouse inherits, broadly, four categories of asset. Each behaves differently, and it is worth knowing which is which before the will is read.

The State Pension

For most couples retiring under the new State Pension rules - that is, those who reached State Pension Age on or after 6 April 2016 - the State Pension is, in essence, an individual entitlement. It is not divisible between spouses, and it is, with limited exceptions, not inheritable. Whatever the deceased was receiving stops in the week of the funeral. The survivor's own State Pension continues as before.

There are some protected elements. "Protected payments" for those whose pre-2016 entitlement exceeded the new flat rate may pass in part to a surviving spouse. The pre-2016 basic State Pension included inheritable elements of Additional State Pension (SERPS, and later S2P), which can still be relevant for older retirees. Each case is its own jigsaw, and the rules are not simple. If you are not sure where you stand, the State Pension forecast at gov.uk is the place to start, and a written statement from the Pension Service is the document to ask for. I am not going to attempt a full summary here because the detail varies materially by date of birth and contribution history; the safe instruction is to ask for it in writing while both spouses are alive to discuss the answer.

The defined benefit pension

The traditional final-salary scheme typically pays a spouse's or partner's pension on death, most often at 50% of the member's pension, though some older schemes pay two-thirds and a few pay 100% for a defined period. The exact figure is in the scheme rules. Public-sector schemes - NHS, teachers, local government, civil service - tend to be the more generous, but they come with their own quirks around remarriage, cohabitation, and the age gap between spouses.

The practical step, while both spouses are alive, is to write to the scheme administrator and ask, in plain English, what the spouse's pension will be in pounds and pence, from what date, and on what conditions. A surprising number of couples have never seen the number written down on headed paper. We strongly suggest you do.

The defined contribution pension

The DC pension passes via the nomination form held by the pension provider, not via the will. This is the single most common point of failure in inheritance planning. Nomination forms made in 1992 still name a sister-in-law nobody has spoken to since the divorce in 2003. The first task, on any DC pension, is to ask for a copy of the current nomination form and check who is named.

Until 6 April 2027, the DC pension passes outside the Inheritance Tax estate. From that date, it is brought inside - the change we covered at length in this article. The spousal exemption still applies, so whatever passes from spouse to spouse remains IHT-free on the first death. The bill, where there is one, lands on the second death and on the estate as a whole.

The ISA, the general account, and the home

Cash, ISAs, general investment accounts and property all pass under the will. ISAs benefit from the Additional Permitted Subscription, which lets the surviving spouse make an additional one-off subscription to their own ISA equal to the value of the deceased's ISA at the date of death - or, by election, the value at the date of transfer. The ISA assets themselves pass to whoever the will directs; the APS allowance simply preserves the tax-sheltered wrapper for the survivor. It is a useful provision and easily missed; we have seen executors fail to claim it more than once.

The home, if it passes between spouses, is IHT-free under the spousal exemption. The Residence Nil-Rate Band, where the home eventually passes to direct descendants on the second death, can shelter a further £350,000 on top of the ordinary nil-rate band (£175,000 per person).

The pattern

On the first death, almost everything passes between spouses without immediate tax friction. On the second death, the IHT thresholds and - from April 2027 - the new pension rules begin to bite. The planning window is the gap between the two. The lever this article is concerned with is the income side of that window: specifically, how to replace the State Pension that disappears on the first death.

/3. The size of the gap

For a couple where both spouses receive the full new State Pension, the loss on the first death is straightforward to put a number on.

The full new State Pension for the 2026-27 tax year is, in round terms, £12,547 per year. For a couple receiving the full amount, household State Pension income is approximately £25,094. After the first death, the surviving spouse continues to receive their own £12,547. The household has lost half of its State Pension overnight.

Two observations:

The first is that household running costs do not fall in step with income. The working rule that retirement advisers tend to use, and there is reasonable supporting data behind it, drawn mainly from the long-running Office for National Statistics work on household expenditure, is that a single person needs roughly 70% of the running cost of a couple, not 50%. So, losing 50% of State Pension income while needing 70% of joint expenditure leaves a real and uncomfortable shortfall. The size of the shortfall depends on the couple's other income, but the direction is unambiguous.

The second observation is that this is a shortfall in inflation-linked, government-guaranteed income. It is precisely the species of income that is hardest, and most expensive, to replace from private resources. The State Pension is uprated each year under the triple lock: the higher of CPI inflation, average earnings growth, or 2.5%, and that uprating has, over the last decade or so, been considerably more generous than the bond market would otherwise have priced. To replicate that promise privately, an investor needs something that indexes with inflation, runs for life, and carries no credit risk.

There are essentially three candidates. Section 4 sets them side by side. Section 5 then takes one of them apart to the last penny.

/4. The three ways to replicate it

There are, broadly, three practical ways to recreate £12,547 of inflation-linked income for a surviving spouse from private capital. None is perfect. Each has a specific cost and a specific risk attached. We will look at them in turn before moving to the worked example in Section 5 – not wishing to spoil anyone’s Saturday morning, this detailed item is stored separately under Investing Tech on our website: https://www.chancerylane.net/investing-tech

Option one. The inflation-linked annuity

The simplest answer is to take a slice of the inherited pension or other capital and buy an inflation-linked annuity in the survivor's name. The insurance company pays a guaranteed monthly income, indexed to a chosen measure (typically RPI, sometimes capped at 3% or 5%), for the rest of the survivor's life.

The strengths are obvious: no investment risk, no longevity risk, no decisions to take in old age, and a single piece of paperwork to retain. The weaknesses are equally clear. The income stops on the survivor's death, with nothing left for the children. The starting income from an RPI-linked annuity is materially lower than from a level annuity at the same price, because the insurer must fund the future indexation. For a survivor genuinely worried about running out of money in a long retirement, that gap is the cost of the certainty, and most clients judge it worth paying. Live quotes vary by provider, health, and the exact indexation chosen, and we would always price the actual case rather than rely on a printed range.

An annuity is an irrevocable purchase of income with 100% loss of capital. Even if you’re annoyed by the inheritance tax on pensions, 60% of something is still much more than 100% of nothing.

Option two. Drawdown via an income strategy

A second answer is to keep the capital invested in a personal pension or general investment account, with a heavy allocation to income-centric investment trusts for the inflation hedge and the reserves and draw the income each year. The strengths are flexibility, inflation management and capital preservation: whatever is unused at death belongs to the estate, and the strategy can be reshaped as the survivor's needs change. The weaknesses are sequencing-of-returns risk - the danger of selling assets to fund income in a falling market, locking in losses that the portfolio cannot recover from - and the simple practical point that a spouse widowed at 72 may not want to be making investment decisions at 82. Drawdown done well requires either active management or active oversight. It is the right answer for many, but it is not a fit-and-forget solution.

Option three. The index-linked gilt held to maturity

The third answer is, to many readers, the least familiar but in some respects the most elegant. The UK government issues index-linked gilts: bonds whose coupon payments and capital redemption value both rise with the Retail Prices Index. (RPI is being aligned with CPIH from 2030, which is a real consideration for any long-dated holding; we will come back to it.) An investor can buy a single index-linked gilt today, hold it to maturity, and receive a known stream of inflation-linked payments backed by the Treasury. There is no investment manager, no insurance company, and no ongoing fee. There is also no annuity-style cross-subsidy from those who die early to those who live long: whatever value remains in the gilt at the date of death belongs to the estate.

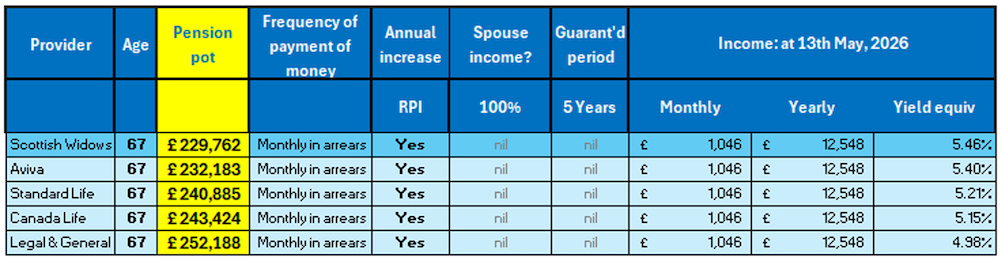

The remaining question is the arithmetic. How much capital does it cost to do this today? What is the actual yield available? How much income can be paid each year, and what happens to the capital at the end? That is what Section 5 sets out, line by line, on the 0.25% Index-Linked Treasury Gilt 2052, which is the longest gilt currently available and the natural building block for a long-dated income replication. It is technical material, but it is not difficult. The conclusion at the end is one most readers will want to hold a pencil over, and given the detail, we have separated it out into an individual article on our investing tech section.

Book a no-obligation chat with us about all things pension, being over 50, and being stuck in the sandwich generation.

020 7390 0670

Two hours, both spouses (while there are still both), no jargon, no pitch. We bring the coffee. You bring the questions, the pension statements, the nomination forms, and whatever index-linked gilt holdings you may already have.

About the author

Doug Brodie is Founder and CEO of Chancery Lane Income Planners. He has specialised in retirement income for over thirty years and is Chartered with both the CISI and CII. This article is general information and not personal advice. Tax rules can change, and the impact of any planning depends on your specific circumstances. Capital is at risk and past performance is not a guide to future returns.